|

Vehicles were the star of the week's calendar showing outstanding strength at both the retail and production levels. The domestic economy may be solid but inflation pressures are very difficult to find, a mix that promises to make for a lively debate at the September FOMC.

Vehicle sales jumped 1.4 percent in July, giving a big lift to the month's retail sales which rose 0.6 percent overall and only 0.4 percent excluding vehicles. The graph compares vehicle sales with retail sales excluding vehicles. The slope for vehicles, the dark line in the graph, has been extending a long climb in contrast to non-vehicle sales which buckled a bit early this year. The relative strength for vehicle sales is also evident in year-on-year sales growth, at 7.0 percent in July for vehicles vs only 1.3 percent excluding vehicles. The latter rate has been below 2.0 percent all year and under 1.0 percent three times. Year-on-year sales of vehicles in contrast have been in the middle to high single digits. Note that vehicle sales make up 21 percent of total retail sales, a ratio that has been on a gradual climb. Vehicle sales jumped 1.4 percent in July, giving a big lift to the month's retail sales which rose 0.6 percent overall and only 0.4 percent excluding vehicles. The graph compares vehicle sales with retail sales excluding vehicles. The slope for vehicles, the dark line in the graph, has been extending a long climb in contrast to non-vehicle sales which buckled a bit early this year. The relative strength for vehicle sales is also evident in year-on-year sales growth, at 7.0 percent in July for vehicles vs only 1.3 percent excluding vehicles. The latter rate has been below 2.0 percent all year and under 1.0 percent three times. Year-on-year sales of vehicles in contrast have been in the middle to high single digits. Note that vehicle sales make up 21 percent of total retail sales, a ratio that has been on a gradual climb.

What has been behind the strength in vehicle sales' Strength in the jobs market is probably the central factor with low gasoline prices perhaps also adding a boost. Consumer confidence surveys are often watched as a leading indicator for vehicle sales though the accompanying graph looks almost the other way around, with the steady climb of vehicle sales contrasting with the topping out underway in the consumer sentiment index. What has been behind the strength in vehicle sales' Strength in the jobs market is probably the central factor with low gasoline prices perhaps also adding a boost. Consumer confidence surveys are often watched as a leading indicator for vehicle sales though the accompanying graph looks almost the other way around, with the steady climb of vehicle sales contrasting with the topping out underway in the consumer sentiment index.

The domestic nature of auto sales is key right now for the economy, giving a big lift to the U.S. factory sector. The dark line of the graph is motor vehicle production as measured in the industrial production report. The light line is industrial production excluding motor vehicles. The contrastustrial production report. Excluding vehicles, manufacturing production rose only 0.1 percent. Buy American is still the watchword for the auto industry which is a plus when the global economy is flat as it is now. The mix between North American-made vehicles and foreign-made vehicles sold in the U.S. has been creeping higher, at 81 percent of total sales as of July. The domestic nature of auto sales is key right now for the economy, giving a big lift to the U.S. factory sector. The dark line of the graph is motor vehicle production as measured in the industrial production report. The light line is industrial production excluding motor vehicles. The contrastustrial production report. Excluding vehicles, manufacturing production rose only 0.1 percent. Buy American is still the watchword for the auto industry which is a plus when the global economy is flat as it is now. The mix between North American-made vehicles and foreign-made vehicles sold in the U.S. has been creeping higher, at 81 percent of total sales as of July.

The factory sector outside autos has been struggling the past year, hit by weakness in energy equipment and by strength in the dollar which is limiting export demand. The nation's exports are concentrated in capital goods and industrial supplies, not vehicles or consumer goods. The industrial production report offers specific readings on consumer goods and business equipment. As the graph shows, growth in business equipment slowed sharply several years ago and is doing no better than tracking along with consumer goods. Year-on-year, production of business equipment is barely in the plus column at 1.1 percent with consumer goods doing a little better at plus 2.3 percent. The factory sector outside autos has been struggling the past year, hit by weakness in energy equipment and by strength in the dollar which is limiting export demand. The nation's exports are concentrated in capital goods and industrial supplies, not vehicles or consumer goods. The industrial production report offers specific readings on consumer goods and business equipment. As the graph shows, growth in business equipment slowed sharply several years ago and is doing no better than tracking along with consumer goods. Year-on-year, production of business equipment is barely in the plus column at 1.1 percent with consumer goods doing a little better at plus 2.3 percent.

There was other evidence in the week's data on the strength of vehicle sales. The producer price report, where pressures were otherwise hard to find, showed outsized price gains in the month for both cars and light trucks. Year-on-year, wholesale prices for vehicles are up in the low to middle single digits, another contrast with the low to middle negative single digits for total finished goods. The Fed will be meeting in September and will perhaps remove stimulus in an effort to stem the risk of future inflation. But expectations for future inflation were tied to the normalization of energy prices which now instead are sinking further, dragging down prices of other commodities and risking further strength for the dollar. The strong dollar been has a central factor deflating import prices as seen in the dark line of the import & export price graph where this year's readings are back to where they were in 2010. There was other evidence in the week's data on the strength of vehicle sales. The producer price report, where pressures were otherwise hard to find, showed outsized price gains in the month for both cars and light trucks. Year-on-year, wholesale prices for vehicles are up in the low to middle single digits, another contrast with the low to middle negative single digits for total finished goods. The Fed will be meeting in September and will perhaps remove stimulus in an effort to stem the risk of future inflation. But expectations for future inflation were tied to the normalization of energy prices which now instead are sinking further, dragging down prices of other commodities and risking further strength for the dollar. The strong dollar been has a central factor deflating import prices as seen in the dark line of the import & export price graph where this year's readings are back to where they were in 2010.

The next graph on prices compares the level of the producer price index with the year-on-year percent change. Prices broke down steeply last year though they did appear to find a floor this spring. But that was before the new breakdown in commodity prices which, together with the slowing in China, does not support the Fed's expectations for a gradual increase in inflation. The price environment may not be turning out as planned. The next graph on prices compares the level of the producer price index with the year-on-year percent change. Prices broke down steeply last year though they did appear to find a floor this spring. But that was before the new breakdown in commodity prices which, together with the slowing in China, does not support the Fed's expectations for a gradual increase in inflation. The price environment may not be turning out as planned.

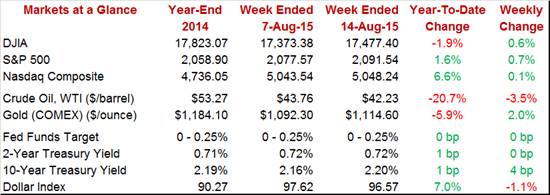

China's devaluation, which hit US markets on Tuesday, is a bolt out of the blue for the FOMC, raising uncertain risks including currency dislocation right at the moment policy makers were nearing liftoff. But US markets were mostly stable with the Dow showing life on Friday to post a weekly gain 0.6 percent. Not stable, however, was oil which fell 3.5 percent on the week to end at $42.23 for WTI. The next target is support at $40 which, if broken, would rattle everyone's forecasts. China's devaluation, which hit US markets on Tuesday, is a bolt out of the blue for the FOMC, raising uncertain risks including currency dislocation right at the moment policy makers were nearing liftoff. But US markets were mostly stable with the Dow showing life on Friday to post a weekly gain 0.6 percent. Not stable, however, was oil which fell 3.5 percent on the week to end at $42.23 for WTI. The next target is support at $40 which, if broken, would rattle everyone's forecasts.

The auto sector has become a leading force for the economy, helping to offset weakness in exports and contraction in the energy sector and helping to give retail sales a major boost heading into the September FOMC. But the doves still have plenty of arguments on their side including the lack of inflation, the second-leg lower for oil prices, and, not least, the uncertain indications from China.

Housing is the week's theme led off Monday by the home builders' housing market index which, at a 10-year high, is expected to extend gains. But less is expected for housing starts & permits on Tuesday and existing homes on Thursday where very strong gains in June are expected to take the edge off July's comparisons. Consumer prices on Wednesday aren't expected to show increasing pressure which, combined with ongoing declines in commodity prices, would point to less pressure on the doves to give into the hawks at the FOMC. Minutes from last month's FOMC will be posted Wednesday afternoon. Of special note will be Thursday's initial jobless claims data where the sample week matches the sample week for the August employment report.

The Empire State Report only showed a small gain in July and isn't expected to show much lift in August either, at a consensus 4.75. New orders in this report have been in the negative column in four of the last five months. Another weak report would raise talk of a lower-than-expected Philly Fed report on Thursday.

Empire State Report - Consensus Forecast for August: 4.75

Range: 3.00 to 6.00

The housing market index is coming off a 10-year high in July at 60 and is expected to add another notch in August to 61. With inventories of new homes thin and with sales going up, optimism among home builders has been growing.

Housing Market Index - Consensus Forecast for August: 61

Range: 59 to 62

Strength for rental units has been driving housing starts & permits sharply higher this year with strength for single-family homes much less pronounced. Forecasters see another rise for starts, up 0.5 percent to a 1.180 million annual rate, but a very sharp 8.4 percent reversal to 1.230 million for permits where the year-on-year rate was up 30 percent in June.

Housing Starts - Consensus Forecast for July: 1.180 million rate

Range: 1.060 to 1.280 million

Housing Permits - Consensus Forecast for July: 1.230 million rate

Range: 1.140 to 1.350 million

The consumer price report did show some pressure in June but less is expected for July with headline expectations at a moderate 0.2 percent gain vs 0.3 percent in June. The core rate is seen repeating a 0.2 percent rise. The year-on-year core rate, at 1.8 percent in June, will get close attention and whether it continues to move toward the Fed's 2 percent. Still, the ongoing decline in oil prices will make this report seem outdated.

Consumer Price Index - Consensus Forecast for July: +0.2%

Range: +0.1% to +0.2%

CPI Less Food & Energy - Consensus Forecast for July: +0.2%

Range: +0.1% to +0.3%

Initial jobless claims are expected to hold near record lows, at 270,000 in the August 15 week. The August 15 week is also the sample week for the monthly employment report which will add special scrutiny to the results.

New Claims, Level - Consensus Forecast for August 15 Week: 270,000

Range: 265,000 to 274,000

The Philadelphia Fed report suddenly burst higher in June to 15.2 but then came back quietly in July to 5.7. Forecasters see a 7.5 reading for August, one that would point to respectable growth for the mid-Atlantic manufacturing sector.

Philadelphia Fed - Consensus Forecast for August: 7.5

Range: 5.0 to 10.5

Existing home sales surged 3.2 percent to an 8-year high in June and are expected to ease back 1.6 percent to a 5.40 million annual rate. Prices in this report have been strong, reflecting a scarcity of available homes for sale and pointing to a seller's market .

Existing Home Sales - Consensus Forecast for July: 5.40 million rate

Range: 5.30 to 5.60

The index of leading economic indicators has been getting a strong boost from housing permits where an expected dip for July, however, is holding down forecasts. The LEI is expected to take a breather in July, up a moderate 0.2 percent.

Index Of Leading Economic Indicators - Consensus Forecast for July: +0.2%

Range: +0.0% to +0.4%

The manufacturing PMI is expected to signal slight acceleration in August, to 54.2 from July's 53.8. The July report noted that manufacturers are focusing their efforts more on the domestic market and less on exports, the result of weak foreign demand together with the effects of the strong dollar.

Manufacturing PMI, Flash - Consensus Forecast for August: 54.2

Range: 54.1 to 55.0

|