|

Growth indicators are weakening and price inflation seems lifeless but the strength of the January employment report, however imperfect, keeps the chances alive for what would be a surprise rate hike at the March FOMC. And don't forget. It was strength in employment and nothing else that made for the initial hike in December. Janet Yellen has plenty to point to if she wants to sound hawkish at Wednesday's semi-annual testimony in Washington. And there are plenty of risks if she sounds dovish. After all, dovish means lack of confidence in the economy, and it's lack of confidence that's been sinking the markets.

The two separate surveys of the January employment report may not be telling exactly the same story, but they definitely aren't telling different stories. First the household survey where the unemployment rate, in a major headline for public policy that can't be ignored, fell 1 tenth to 4.9 percent for the best reading so far this cycle, since 2008. This was no surprise but what was a surprise is a further 1 tenth rise in the labor participation rate to 62.7 percent. This rate combines those that already have work along with those looking for work. As seen in the dark line of the graph, this reading, which has been in a long disappointing descent, is suddenly on the climb with a 3 tenths gain since September. More people looking for work, and more people having work, is a simple equation for the hawks that equals — Wage Inflation. The two separate surveys of the January employment report may not be telling exactly the same story, but they definitely aren't telling different stories. First the household survey where the unemployment rate, in a major headline for public policy that can't be ignored, fell 1 tenth to 4.9 percent for the best reading so far this cycle, since 2008. This was no surprise but what was a surprise is a further 1 tenth rise in the labor participation rate to 62.7 percent. This rate combines those that already have work along with those looking for work. As seen in the dark line of the graph, this reading, which has been in a long disappointing descent, is suddenly on the climb with a 3 tenths gain since September. More people looking for work, and more people having work, is a simple equation for the hawks that equals — Wage Inflation.

And there are other indications of strength in the report including a convincing rise in the workweek and a 0.5 percent monthly spike in average hourly earnings. Though this is the second strongest gain of the whole cycle, back to 2008, earnings may have been skewed higher by state-level minimum wage increases. And strength isn't confirmed by the year-on-year rate which, as seen in the line on the graph, is stuck at only 2.5 percent. The Fed is counting on wage pressures to begin offsetting deflationary pressures elsewhere, but 2.5 percent probably isn't enough. Hourly earnings will have to show further strength in the February jobs report before helping the hawks much at the March FOMC. And the payroll side of the January report is no help at all to the hawks, with nonfarm payroll growth coming in at only 151,000 and much lower than prior months. But even here, 151,000 isn't really that bad. And there are other indications of strength in the report including a convincing rise in the workweek and a 0.5 percent monthly spike in average hourly earnings. Though this is the second strongest gain of the whole cycle, back to 2008, earnings may have been skewed higher by state-level minimum wage increases. And strength isn't confirmed by the year-on-year rate which, as seen in the line on the graph, is stuck at only 2.5 percent. The Fed is counting on wage pressures to begin offsetting deflationary pressures elsewhere, but 2.5 percent probably isn't enough. Hourly earnings will have to show further strength in the February jobs report before helping the hawks much at the March FOMC. And the payroll side of the January report is no help at all to the hawks, with nonfarm payroll growth coming in at only 151,000 and much lower than prior months. But even here, 151,000 isn't really that bad.

Domestic-based service demand is the foundation of the jobs market but, in more bad news for the hawks, the service sector may be slowing. Service-producing payrolls rose a very soft 118,000 and were perhaps the weakest headline of the January employment report. Other soft indications include the ISM's non-manufacturing index which, in data that came out at mid-week, fell very sharply to 53.5 to signal the weakest rate of month-to-month growth since all the way back in July 2012. Growth in the report's employment index also slowed sharply to correctly signal the slowdown in service payrolls. Output also slowed as did imports with the latter signaling business caution. But all is not lost. New orders, the most important of any of the report's readings, held in at a very solid 56.5. Domestic-based service demand is the foundation of the jobs market but, in more bad news for the hawks, the service sector may be slowing. Service-producing payrolls rose a very soft 118,000 and were perhaps the weakest headline of the January employment report. Other soft indications include the ISM's non-manufacturing index which, in data that came out at mid-week, fell very sharply to 53.5 to signal the weakest rate of month-to-month growth since all the way back in July 2012. Growth in the report's employment index also slowed sharply to correctly signal the slowdown in service payrolls. Output also slowed as did imports with the latter signaling business caution. But all is not lost. New orders, the most important of any of the report's readings, held in at a very solid 56.5.

Construction, which is not defined as a service, is also included in the ISM non-manufacturing sample and it generally showed strength in the January report. But construction payrolls in the employment report did not show much strength, rising only 18,000 vs much larger gains in prior months. Also proving soft were data on construction spending, inching only 0.1 percent higher in December and following prior declines. The good news is on the residential side where construction spending rose a very strong 0.9 percent on the month led once again by multi-family units. But single-family units have also been strong, up a year-on-year 8.7 percent. Less strong, however, is spending on non-residential construction, at least for December when it fell 2.1 percent on the month for a second straight decline. Construction, which is not defined as a service, is also included in the ISM non-manufacturing sample and it generally showed strength in the January report. But construction payrolls in the employment report did not show much strength, rising only 18,000 vs much larger gains in prior months. Also proving soft were data on construction spending, inching only 0.1 percent higher in December and following prior declines. The good news is on the residential side where construction spending rose a very strong 0.9 percent on the month led once again by multi-family units. But single-family units have also been strong, up a year-on-year 8.7 percent. Less strong, however, is spending on non-residential construction, at least for December when it fell 2.1 percent on the month for a second straight decline.

Showing increasingly less life is the factory sector. Factory orders for December fell a sharp 2.9 percent while the ISM's new orders index for manufacturing, at 51.5 as seen in the line of the accompanying graph, remained on the wrong side of the monthly expansion-contraction line. Don't be alarmed but this line isn't actually at 50. More precisely it's at 52.2 as calculated by the government in inflation-adjusted dollars. This is the sixth month below this bar and, though improving from the prior two months, new orders are pointing to a soft first quarter for the factory sector. And turning back to the factory orders report for one last detail, capital goods orders are way down in what is yet another indication of falling business confidence. Showing increasingly less life is the factory sector. Factory orders for December fell a sharp 2.9 percent while the ISM's new orders index for manufacturing, at 51.5 as seen in the line of the accompanying graph, remained on the wrong side of the monthly expansion-contraction line. Don't be alarmed but this line isn't actually at 50. More precisely it's at 52.2 as calculated by the government in inflation-adjusted dollars. This is the sixth month below this bar and, though improving from the prior two months, new orders are pointing to a soft first quarter for the factory sector. And turning back to the factory orders report for one last detail, capital goods orders are way down in what is yet another indication of falling business confidence.

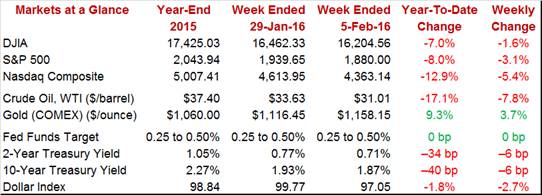

When did I go wrong? Well, if you're the Fed, some would say December 16, 2015 when lift-off began. Since then, the Dow (in what may of course be complete coincidence) has fallen 7.5 percent in wild trading. The new slogan should be: Don't fight the Fed — no matter how incremental they say the move is. Expectations are in a fog for the next hike, perhaps as early as June or perhaps not until next year. The pushing back of expectations, accelerated by global-risk headlines from New York's William Dudley, made for a 2.7 percent weekly decline in the dollar index. This is a very steep loss for the dollar and one that won't upset exporters. And pointing perhaps to further cooling for the dollar are interest rates which keep coming down as investor confidence keeps coming down. Instead of going up like it was supposed to after liftoff, the 2-year yield, at 0.71 percent, is down a shocking 34 basis points so far this year. When did I go wrong? Well, if you're the Fed, some would say December 16, 2015 when lift-off began. Since then, the Dow (in what may of course be complete coincidence) has fallen 7.5 percent in wild trading. The new slogan should be: Don't fight the Fed — no matter how incremental they say the move is. Expectations are in a fog for the next hike, perhaps as early as June or perhaps not until next year. The pushing back of expectations, accelerated by global-risk headlines from New York's William Dudley, made for a 2.7 percent weekly decline in the dollar index. This is a very steep loss for the dollar and one that won't upset exporters. And pointing perhaps to further cooling for the dollar are interest rates which keep coming down as investor confidence keeps coming down. Instead of going up like it was supposed to after liftoff, the 2-year yield, at 0.71 percent, is down a shocking 34 basis points so far this year.

The economy is getting off to a slow start this year in what may ultimately reflect the initial impact of financial market stress. But it's no time to panic, at least not yet. The labor market continues its steady build to full employment and the Fed has yet to abandon, at least up to this writing, guidance for an ongoing series of rate hikes.

Economic data will take a backseat to Janet Yellen's semi-annual testimony in Washington which starts on Wednesday. Will she cite the strengths of the January and keep alive a rate for the March FOMC? Or will she push expectations, perhaps citing rising global risks to the economic outlook. The week's key data come at week's end with import & export prices, where yet another sweep of deflationary signals are expected, and also retail sales which are expected, outside another month of contraction for gasoline stations, to show improvement including for vehicles.

The small business optimism index has been on the climb with key components − job openings and plans to increase employment − showing solid strength. Capital investment, which is directly related to future employment, has also been positive. The Econoday consensus is calling for a slight dip to 94.9 in the January index vs 95.2 in December.

Small Business Optimism Index - Consensus Forecast for January: 94.9

Range: 93.8 to 95.6

Wholesale inventories, due to soft demand, have been on the decline. Inventories fell a sizable 0.3 percent in the last report for November but sales fell even more sharply, down 1.0 percent to drive the stock-to-sales ratio to 1.32 from 1.31. Further destocking is expected for December with the Econoday consensus at minus 0.1 percent.

Wholesale Inventories, M/M Chg. - Consensus Forecast for December: -0.1%

Range: -0.4% to +0.1%

Initial jobless claims have been on the climb as have continuing claims, signaling weakness for what is still however a very solid labor market. The Econoday consensus is calling for a 4,000 fall in initial claims for the February 6 week to 281,000.

Initial Jobless Claims - Consensus Forecast for February 6 week: 281,000

Range: 272,000 to 290,000

Held back by vehicle sales, retail sales began to slow and finally contract going into year-end. But sales of vehicles, based on last week's data from manufacturers, look to be a positive for January with the Econoday consensus calling for a moderate 0.2 percent headline gain following a 0.1 percent decline in December. Declines in gasoline sales, the result of falling prices, have been skewing readings lower in this report. Outside of vehicles and gasoline, a respectable plus 0.3 percent gain is expected. Strength in this report, which would confirm the engagement of the consumer, is critical for the first-quarter outlook.

Retail Sales - Consensus for January: +0.2%

Range: -0.3% to +0.4%

Retail Sales Ex-Autos - Consensus for January: +0.1%

Range: -0.2% to +0.3%

Retail Sales Ex-Autos Ex-Gas - Consensus for January: +0.3%

Range: +0.1% to +0.6%

Falling commodity prices and weak demand abroad have led to a long series of deep declines for import & export prices with the import side further pressured by the strength of the dollar which makes imports even cheaper. The Econoday consensus is calling for a very steep 1.4 percent decrease for import prices in January, which would be the 7th drop in a row, as well as a 0.6 percent decrease for export prices which would be the 6th drop in a row. Weakness in this report has not been confined to raw materials as contraction for finished goods prices has been building steam.

Import Prices, M/M Chg - Consensus Forecast for January: -1.4%

Range: -2.2% to -0.7%

Export Prices, M/M Chg - Consensus Forecast for January: -0.6%

Range: -1.0% to -0.2%

Consumer confidence measures have been steady and firm and have been pointing to no immediate psychological impact from global stress and losses in the domestic stock market. The consumer sentiment index is expected to come in at 92.5 for the flash February reading vs 92.0 for final January and January's flash of 93.3. An important detail will be inflation expectations and the effect of still falling gasoline prices, a reading that is closely watched by Federal Reserve policy makers. Resiliency and patience for the domestic consumer, who is the single-most pillar of the U.S economy, would point to unexpected strength for the first quarter.

Consumer Sentiment, Flash - Consensus for February: 92.5

Range: 91.0 to 93.5

Business inventories have been on the decline, not the result of strong demand but due to concerted destocking as sales have been soft. After falling 0.2 percent in November and 0.1 percent in October, the Econoday consensus is calling for a small rise in December of 0.1 percent. Slowing inventories are a negative for GDP but, given slowing demand, are a positive for future production and employment.

Business Inventories - Consensus for December: +0.1%

Range: -0.2% to +0.3%

|