|

The Week Ahead: Highlights

Asia-Pacific Preview

RBA Rate Hike Expected

By Brian Jackson, Econoday Economist

The Reserve Bank of Australia policy meeting will be the

main focus with officials widely expected to raise policy rates again after the

25 basis point increase announced last month. CPI data published since then

have shown headline inflation steady at 3.8 percent in January, above the RBA's

target range of two percent to three percent for the fifth consecutive month,

Officials have clearly indicated in their public commentary that a rate hike

will be considered at this meeting, and the impact of the Iran conflict on fuel

prices have added to concerns about the inflation outlook. Any guidance about

additonal future rate hikes will also watched closely.

Chinese activity data for January and February will also be published next

week. Separate data for these two months are not published because of the

impact of the timing of lunar new year holidays. so next week's data will

provide a clearer indication of how the Chinese economy has begun the year.

Official PMI survey data showed weak conditions in both months but the

private-sector PMU survey showed a soldi improvement in February.

Tian's central bank will hold its quarterly policy meeting with officials

likely to keep rates on hold again. Other indicators scheduled for release next

week include Australian labour market data, New Zealand GDP and trade data, and

Hong Kong inflation data.

Europe Preview

Rate Decisions and Trade Results Headline Week Ahead

By Marco Babic, Econoday Economist

Last week was a busy one, with the escalating conflict in

the middle east, and the Trump administration seeking new avenues to impose

tariffs on the US's trading partners after the initial ones were largely deemed

illegal. To add to that, the administration said it could be some time before

any refunds are issued, so there will unlikely be a quick near-term infusion of

money into the economy.

A slew of countries release their trade data next week: The

Netherlands, Norway, Belgium, Switzerland, and Italy. While it is clearly far

too early for the current events to appear in the trade numbers, they will

nevertheless provide some guidance as to how the flows of goods and services

have fared at the start of the year. Moreover, they could provide clues as to

whether there is underlying economic weakness.

On Thursday, the European Central Bank and the Swiss

National Bank will make public their decision on interest rates. The ECB has

been cautious in recent meetings as has the SNB, and rates are likely to be

kept on hold once again. In the case of Switzerland, a rate cut would be

another foray into the world of negative interest rates. And while the SNB will

make a move should economic conditions warrant, they are still more likely to

err on the side of caution.

What will be of heightened interest is what the policy

makers at both institutions have to say about economic conditions, the conflict

and inflation. Price increases have been in the comfort zone of the ECB for

some time, as have those in Switzerland. However, in February, the moved higher

in both the Eurozone and Switzerland. Once again inflation is highly likely to

be high on the list of talking points among respective governing councils.

Clearly the events unfolding in the Middle East are adding

inflationary pressures that are not yet evident in the data and will be

something to consider. Add to that the downward economic pressures, there is a

real danger of stagflation becoming a reality. Still, Europe has an advantage

with the Euro and Swiss Franc both relatively strong versus the dollar in which

crude oil is prices. Energy prices have for some time been a mitigating factor

for inflation in Europe generally, but that is about to change.

US Preview

FOMC Meeting Is Main Event

By Theresa Sheehan, Econoday Economist

In the March 16 week, attention will be focused on the

Tuesday-Wednesday FOMC meeting, the release of the meeting statement and update

to the summary of economic projections (SEP) at 14:00 ET on Wednesday, and

Chair Jerome Powell's press conference at 14:30 ET on Wednesday.

The FOMC decision will be made against a backdrop of

conflicting data reports on conditions in the labor market and an incomplete

picture of inflation. The February 28 attack on Iran quickly drove energy

prices higher and generated heightened geopolitical uncertainty which will show

up in coming months. The FOMC faces renewed "tension" in the dual mandate

between supporting maximum employment and achieving prices stability in the

context of the Fed's 2 percent inflation objective.

On the employment side, the data about the labor market

suggests that the "no hire, no fire" situation persists. The drop of 92,000 in

nonfarm payrolls in February could be a one-off related to cold weather

preventing outdoor occupations from working and a major strike by nurses in New

York. However, the onset of military actions in the Middle East without a clear

objective or conditions to end the conflict mean increased risks to the

economic outlook. Businesses and consumers will respond with caution, especially

where rapidly rising energy costs cut into discretionary purchases. This could

extend to the jobs market with delays in bringing on new hires by businesses

and households wondering about job security.

On the price stability side, Fed policymakers understand

that oil prices have surged in direct response to the war and should fall again

when peace returns and production resumes. Nonetheless, it takes more time for

prices to come down than it does for them to go up. With the duration of the

conflict an open question, there will be visible effects in the inflation

indicators. How much and how long remains to be seen. The March report on the

CPI is not until 8:30 ET on April 10 and the PPI until Aprill 14 at 8:30 ET.

These will only show the first wave of inflation impacts. If the war drags on,

it will keep fuel prices higher and household discretionary spending lower.

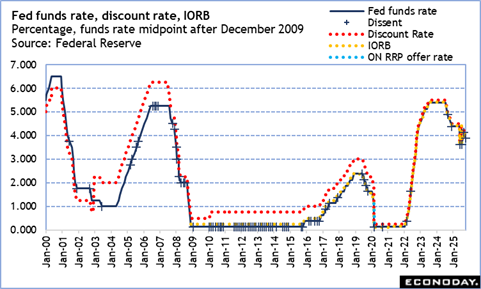

The FOMC meetings have ended with at least one dissenting

vote in favor of a rate cut since July 30, 2025. Dissenters have seen greater

risks to maximum employment and/or that tariff-driven inflation is passing

through the supply chain but not a source of entrenched inflation. Since the

last rate cut of 25 basis points on December 10, 2025, a majority of FOMC

voters have been willing to wait on the economic data for greater clarity as it

catches up after the government shutdown of October 1-November 12. A dissent

from at least one FOMC member is to be expected - Governor Stephen Miran - and

possibly one more - Governor Christopher Waller. Both will weigh the risks to

employment as greater than that of inflation.

Any clarity gained in the intermeeting period has been

muddied by the advent of war on Iran. While a rate cut is possible at the

upcoming meeting, more likely the FOMC will hold off. Powell has previously

said that the current fed funds target rate range of 3.50 to 3.75 percent is

within reach of neutral. Most on the FOMC will prefer to not cut now and have

to retrace it later should inflation become more entrenched.

The meeting will include the quarterly update to the summary

of economic projections (SEP). This will have to be parsed carefully. In

uncertain times the forecasts are more subject to revision later. Even more

than usual, the forecasts should not be read as messaging about FOMC

intentions.

When Powell takes the podium as his press briefing he will

reiterate that monetary policy is not on a preset path and that the FOMC is

committed to delivering on its dual mandate through a balanced approach. In

some ways, he will be setting the stage for his semiannual monetary policy

testimony which has yet to take place. Powell can also expect to be peppered

with questions about his plans with his term as Chair nearing its end in

mid-May. This happened at his last press briefing and he deflected with humor.

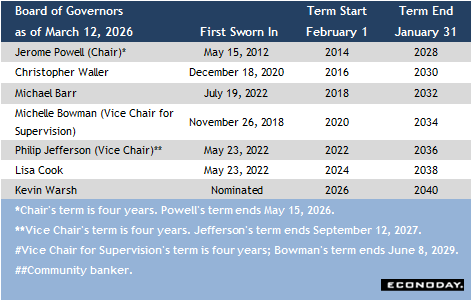

In all likelihood, he will still be chair at the April 28-29

meeting even if the confirmation hearings for Kevin Warsh are done and Warsh is

confirmed as a governor to replace outgoing Miran. Once his four-year term as chair

is done, Powell can remain as a governor until that term is complete on January

31, 2028.

The Week Ahead: Econoday Consensus Forecasts

Monday

China Fixed Asset Investment for January/February (Mon

1000 CST; Mon 0200 GMT; Mon 2200 EDT)

Consensus Forecast, Year to Date on Y/Y Basis: -3.0%

Consensus Range, Year to Date on Y/Y Basis: -4.2% to 2.0%

After an ugly 3.8 percent drop in December, the consensus

sees a slightly less bad contraction at minus 3.0 percent on year for

January/February. Extraordinary to see these declines after years of solid

gains.

China Industrial Production for January/February (Mon

1000 CST; Mon 0200 GMT; Mon 2200 EDT)

Consensus Forecast, Y/Y: 5.0%

Consensus Range, Y/Y: 5.0% to 6.1%

The consensus sees output growth pretty steady, up 5.0

percent on year the January-February after rising 5.2 percent in December.

China Retail Sales for January/February (Mon 1000

CST; Mon 0200 GMT; Mon 2200 EDT)

Consensus Forecast, Y/Y: 2.1%

Consensus Range, Y/Y: 1.1% to 4.4%

A bit of a pickup expected with retail sales up 2.1 percent

on year versus only 0.9 percent in December.

Canada Housing Starts for February (Mon 0815 EDT; Mon

1215 GMT)

Consensus Forecast, Annual Rate: 257K

Consensus Range, Annual Rate: 230K to 260K

Starts expected to rebound to 257K rate in February after

dropping to 238K in January.

Canada CPI for February (Mon 0830 EDT; Mon 1230 GMT)

Consensus Forecast, CPI - M/M: 0.6%

Consensus Range, CPI - M/M: 0.1% to 0.7%

Consensus Forecast, CPI - Y/Y: 1.9%

Consensus Range, CPI - Y/Y: 1.7% to 2.1%

CPI expected up 0.6 percent on month (NSA) in February and 1.9

percent on year after no change on month and rising 2.3 percent on year in

January.

US Empire State Manufacturing Index for March (Mon

0830 EDT; Mon 1230 GMT)

Consensus Forecast, Index: 3.9

Consensus Range, Index: -5.0 to 5.0

The consensus sees the index at 3.9 for March versus 7.1 in

February, suggesting slower growth.

US Industrial Production for February (Mon 0915 EDT; Mon

1315 GMT)

Consensus Forecast, Industrial Production - M/M: 0.1%

Consensus Range, Industrial Production - M/M: -0.3%

to 0.7%

Consensus Forecast, Manufacturing Output - M/M: 0.2%

Consensus Range, Manufacturing Output - M/M: 0.1% to 0.3%

Consensus Forecast, Capacity Utilization Rate: 76.2%

Consensus Range, Capacity Utilization Rate: 75.9% to 76.5%

Output seen up 0.1 percent in February after rising 0.7

percent in January.

US Housing Market Index for March (Mon 1000 EDT; Mon

1400 GMT)

Consensus Forecast, Index: 37

Consensus Range, Index: 32 to 38

Not much recovery expected in homebuilder sentiment with the

index nearly flat at 37 from very weak 36 a month ago.

Tuesday

Australia RBA Announcement (Tue 1430 AEDT; Tue 0330

GMT; Mon 1130 EDT)

Consensus Forecast, Change: +10 bp

Consensus Range, Change: 0 bp to 10 bp

Consensus Forecast, Level: 3.85%

Consensus Range, Level: 3.85% to 4.10%

Hawkish comments from RBA officials prompted most forecasters

to move up expectations for another 25 bp rate hike to the March meeting from

May. The minority view still looks for no change.

Italy CPI for February (Tue 0900 CET; Tue 0800 GMT; Tue

0400 EDT)

Consensus Forecast, M/M: 0.8%

Consensus Range, M/M: 0.6% to 0.8%

Consensus Forecast, Y/Y: 1.6%

Consensus Range, Y/Y: 1.6% to 1.6%

The consensus forecast sees no revision from the preliminary

gains of 0.8 percent on month and 1.6 percent on year in the February final.

Germany ZEW survey

Germany ZEW Survey for March (Tue 1100 CET; Tue 1000

GMT; Tue 0600 EDT)

Consensus Forecast, Current Conditions: -64.0

Consensus Range, Current Conditions: -68.0 to -63.7

Consensus Forecast, Economic Sentiment: 40.5

Consensus Range, Economic Sentiment: 30.0 to 55.0

The consensus looks for a weaker reading at minus 64.0 for

current conditions and 40.5 for sentiment versus minus 65.9 and 58.3,

respectively, in the prior month.

US Pending Home Sales Index for February (Tue 1000

EDT; Tue 1400 GMT)

Consensus Forecast, M/M: -1.0%

Consensus Range, M/M: -1.0% to 0.2%

Sales depressed, expected down 1.0 percent on month in

February after a decline of 0.8 percent in January.

Wednesday

Japan Merchandise Trade for February (Wed 0850 JST;

Tue 2350 GMT; Tue 1950 EDT)

Consensus Forecast, Balance: ¥-521.80 B

Consensus Range, Balance: ¥-660.00 B to ¥49.80 B

Consensus Forecast, Imports - Y/Y: 14.5%

Consensus Range, Imports - Y/Y: 9.1% to 16.2%

Consensus Forecast, Exports - Y/Y: 1.6%

Consensus Range, Exports - Y/Y: -3.5% to 4.0%

Japanese export values are projected to increase for a sixth

straight month in February

but are expected to decelerate sharply from a month earlier,

when rush shipments

ahead of the Lunar New Year prompted unexpectedly robust

trading activity. A sharp

increase in imports is expected to push the country's trade

balance into a deficit for the

second straight month.

In reaction to the sharp rise in the previous month and the

fact that this year's Lunar

New Year holiday in mainland China lasted beyond

mid-February - from Feb. 16 to 23

- trading activity with the world's second-largest economy

is expected to slow

considerably during the month, leaving exports seen rising

only 1.6% in February after

surging 16.8% in January.

In contrast, imports are expected to jump 14.5% in February

in reaction to a revised

2.4% decline a month earlier, following decreases for five

straight months through

January. Large increases in imports are expected in

semiconductor-related electronic

components, non-ferrous metals and mobile phones, while no

major items are seen

posting a significant decline during the month. Taking these

moves into account,

Japan's customs-cleared trade balance is expected to post a

deficit of ¥521.8 billion in

February for the second straight month.

Eurozone HICP for February (Wed 1100 CET; Wed 1000

GMT; Wed 0600 EDT)

Consensus Forecast, HICP - Y/Y: 1.9%

Consensus Range, HICP - Y/Y: 1.9% to 1.9%

Consensus Forecast, Narrow Core - Y/Y: 2.4%

Consensus Range, Narrow Core - Y/Y: 2.4% to 2.4%

No revision from the flash at 1.9 percent and 2.4 percent

narrow core for the final HICP.

US PPI-Final Demand for February (Wed 0830 EDT; Wed 1230

GMT)

Consensus Forecast, PPI-FD - M/M: 0.3%

Consensus Range, PPI-FD - M/M: 0.1% to 0.3%

Consensus Forecast, Ex-Food & Energy - M/M: 0.3%

Consensus Range, Ex-Food & Energy - M/M: 0.2% to 0.5%

Wholesale prices seen up 0.3 percent on month for total and ex-food

& energy

Canada Bank of Canada Announcement (Wed 0945 EST; Wed

1345 GMT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 2.25%

Consensus Range, Level: 2.25% to 2.25%

Forecasters expect the bank to keep rates on hold at 2.25

percent this time but the odds of a rate hike later in the year have ticked up

with oil prices.

US Factory Orders for January (Wed 1000 EDT; Wed 1400

GMT)

Consensus Forecast, M/M: 0.1%

Consensus Range, M/M: -0.6% to 0.9%

The consensus sees orders nearly flat with an increase of

0.1 percent.

US FOMC Announcement (Wed 1400 EDT; Wed 1800 GMT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Federal Funds Rate - Target Range: 3.50-3.75%

Consensus Range, Federal Funds Rate - Target Range: 3.50-3.75%

to 3.50-3.75%

Forecasters see no action at this meeting as circumstances

are too uncertain with the Iran war under way and oil prices spiking.

Thursday

New Zealand GDP for Fourth Quarter (Thu 1045 NZDT;

Wed 2145 GMT; Wed 1745 EDT)

Consensus Forecast, Q/Q: 0.5%

Consensus Range, Q/Q: 0.5% to 0.5%

Consensus Forecast, Y/Y: 1.7%

Consensus Range, Y/Y: 1.7% to 1.7%

The consensus looks for GDP up 0.5 percent on quarter in Q4

and 1.7 percent on year versus 1.1 percent and 1.3 percent in Q3.

Japan Machinery Orders for January (Thu 0850 JST; Wed

2350 GMT; Wed 1950 EDT)

Consensus Forecast, M/M: -11.6%

Consensus Range, M/M: -13.9% to -5.5%

Consensus Forecast, Y/Y: 9.7%

Consensus Range, Y/Y: 6.2% to 16.0%

Core machinery orders are projected to fall 11.6% on the

month in January after

soaring 19.1% in the previous month, which was also

supported by ongoing services-

sector demand for computers amid an automation and

digitization drive aimed at

alleviating labor shortages. On a year-on-year basis, core

orders, excluding those from

electric utilities and for ships, are expected to rise 9.7%,

after gaining 16.8% in

December.

Australia Labour Force Survey for February (Thu 1130

AEDT; Thu 0030 GMT; Wed 2030 EDT)

Consensus Forecast, Employment - M/M: 32K

Consensus Range, Employment - M/M: 10K to 40K

Consensus Forecast, Unemployment Rate: 4.1%

Consensus Range, Unemployment Rate: 4.1% to 4.1%

The consensus sees a moderate 32K rise in employment and no

change in the jobless rate flat at 4.1 percent.

(Thu 1130 JST; Thu 0230 GMT; Thu 2230 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 0.75 %

Consensus Range, Level: 0.75 % to 0.75 %

No change is the call from the BOJ.

UK Labour Market Report for March (Thu 0700 GMT; Tue

0300 EDT)

Consensus Forecast, ILO Unemployment Rate: 5.3%

Consensus Range, ILO Unemployment Rate: 5.2% to 5.3%

The jobless rate is expected up at 5.3 percent from 5.2

percent a month earlier.

Switzerland SNB Monetary Policy Assessment for March (Thu

0830 CET; Thu 0730 GMT; Thu 0330 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 0.0%

Consensus Range, Level: 0.0% to 0.0%

The bank is expected to keep rates at zero with fx

intervention its tool of choice to hold down the rising Swiss franc.

UK BoE Announcement and Minutes (Thu 1200 GMT; Thu 0800

EDT)

Consensus Forecast, Bank Rate - Change: 0 bp

Consensus Range, Bank Rate - Change: 0 bp to 0 bp

Consensus Forecast, Bank Rate - Level: 3.75%

Consensus Range, Bank Rate - Level: 3.75% to 3.75%

The consensus sees no action pending clarity on oil prices.

US Jobless Claims for Week03/14 (Thu 0830 EDT; Thu 1230

GMT)

Consensus Forecast, Initial Claims - Level: 215K

Consensus Range, Initial Claims - Level: 215K to 220K

Claims seen at 215K in the latest week versus 213K in the

previous week as new claims remain subdued.

US Philadelphia Fed Manufacturing Index for March (Thu

0830 EDT; Thu 1230 GMT)

Consensus Forecast, Index: 5.5

Consensus Range, Index: 2.0 to 11.6

As with Empire manufacturing, slower growth seen with the

index barely positive at 5.5 in March versus 16.3 in February.

Eurozone ECB Announcement (Thu 1415 CEST; Thu 1315

GMT; Thu 0915 EDT)

Consensus Forecast, Refi Rate Change: 0 bp

Consensus Range, Refi Rate Change: 0 bp to 0 bp

Consensus Forecast, Refi Rate Level: 2.15 %

Consensus Range, Refi Rate Level: 2.15% to 2.15%

Too much uncertainty for the ECB to make any changes now.

US New Home Sales for January (Thu 1000 EDT; Thu 1400

GMT)

Consensus Forecast, Annual Rate: 728K

Consensus Range, Annual Rate: 710K to 800K

Already soft sales seen weaker at an annual 728K in January

versus 745K in December.

Friday

China Loan Prime Rate for March (Fri 0915 CST; Thu

0115 GMT; Thu 2115 EDT)

Consensus Forecast, 1-Year Rate - Change: 0 bp

Consensus Range, 1-Year Rate - Change: 0 bp to 0 bp

Consensus Forecast, 1-Year Rate - Level: 3.00%

Consensus Range, 1-Year Rate - Level: 3.00% to 3.00%

Consensus Forecast, 5-Year Rate - Change: 0 bp

Consensus Range, 5-Year Rate - Change: 0 bp to 0 bp

Consensus Forecast, 5-Year Rate - Level: 3.50%

Consensus Range, 5-Year Rate - Level: 3.50% to 3.50%

The PBOC has not signaled any change.

Canada Retail Sales for January (Fri 0830 EDT; Fri 1230

GMT)

Consensus Forecast, M/M: 1.5%

Consensus Range, M/M: 0.3% to 1.5%

Forecasters agree with Stats Canada's preliminary estimate

calling for sales up 1.5 percent in January.

|