|

The Week Ahead: Highlights

Asia-Pacific Preview

Australia CPI -- Heating Up

By Brian Jackson, Econoday Economist

Monthly Australian CPI data for February will be the main

focus in the Asia-Pacific region. Headline inflation has been above the Reserve

Bank of Australia's target range of two percent to three percent for five

consecutive months, prompting another rate hike last week. Week ahead data

pre-dates the spike higher in fuel prices caused by the Iran conflict but will

likely show that price pressures had remained strong before recent

developments.

The March flash PMI survey for India may provide an early

indication of any impact of the Iran conflict on activity and sentiment in the

region. Singapore will also publish inflation and industrial production data

for February next week, while Taiwan will report industrial production data and

Hong Kong will report trade data.

Europe Preview

Economic Reports to Show First Look at Middle East

Effects

By Marco Babic, Econoday Economist

Economic data from Europe in the week ahead will provide the

first insights as to how the conflict in the Middle East is being digested,

with March data on offer. The main event will be the flash PMI composite

reports from the UK, Germany, France which will be among the first data that

fully incorporate data from March when the conflict escalated. Last week,

central banks in Europe set the tone, saying the conflict will lead to

inflationary pressures and that the global economy was under threat.

While that may seem obvious, it is worth noting that the

European Central Bank, Bank of England, and Swiss National Bank were quick to

make assessments. In addition, there have been some company reports, Germany's

chemical giant BASF comes to mind, where they will have to raise prices due to

the cost if inputs for critical chemicals.

With that, the PMI reports will provide clues as to where

sentiment is headed - presumably lower - and to what degree. The PMI reports

don't provide detailed numerical component breakdowns, but the direction of the

overall numbers will provide a view on how other indicators will develop. In

addition to the PMIs, Germany's widely followed Ifo business sentiment index

will be released as well and could give some insight into the countries

chemicals sector. Consumer sentiment for April will also be reported, which

will perhaps indicate how consumers in Europe's largest economy are reacting to

the geopolitical developments.

Finally, France and Italy also report their results for

business sentiment. While sentiment has been subdued due to weak order books

and working off inventories, there has been a degree of optimism that things

will improve over the coming twelve months, particularly in France. With the

recent developments, that optimism could prove to be very well misplaced.

US Preview

District Fed Manufacturing/Services Reports May Show

Initial Impact from Iran War

By Theresa Sheehan, Econoday Economist

The March 23 week includes some of the first monthly data

that could start to clarify the economic impacts of the Iran war that began on

February 28.

Several of the five Fed district bank surveys of

manufacturing and services for March are set for release in the week. The

surveys are taken in the first half of the month, so will only encompass

initial reactions to the war at a time when its duration and geographic scope

were largely unknown. This is only the first wave of data and needs to be read

with caution.

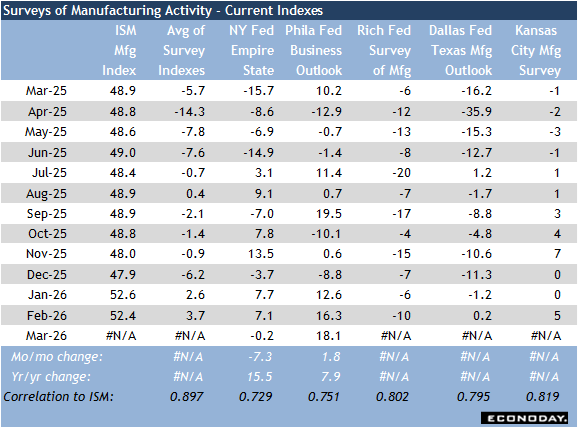

The manufacturing surveys from the New York and Philadelphia

districts for March have already been reported. Their respective general

business conditions indexes moved in opposite directions. The New York index

fell 7.3 points to minus 0.2, erasing two months of modest expansion. The

Philadelphia index is up 1.8 points to 18.1 to its highest reading since

September 2025. The current activity measures for the Richmond and Kansas

districts are set for release at 10:00 ET on Tuesday and 11:00 ET on Thursday.

The Dallas Fed manufacturing survey will not be available until Monday, March

30 at 10:30 ET.

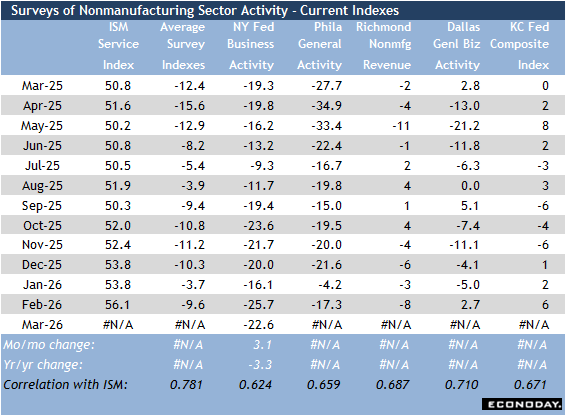

The service sector survey for March from the New York has

been reported with the current business activity up slightly to minus 22.6,

still consistent with contracting conditions. The non-manufacturing activity

indexes from the Philadelphia, Richmond, and Kansas City districts will be

released on Tuesday at 8:30 ET, Tuesday at 10:00 ET, and Friday at 11:00 ET,

respectively. The Dallas Fed current service sector activity index will be

released on Tuesday, March 31 at 10:30 ET.

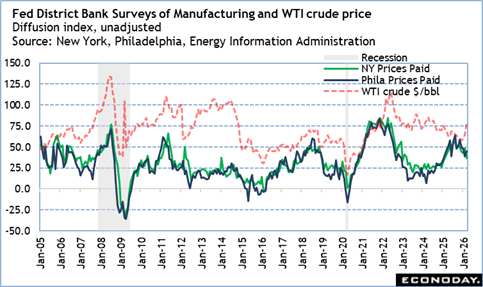

What may be more important in the various surveys is what is

happening with the prices paid/input costs indexes. There is likely some

immediate reaction to the surge in oil prices in the first weeks of March. It

remains to be seen if the upward price pressure is sustained as higher energy

costs pass through the supply chain.

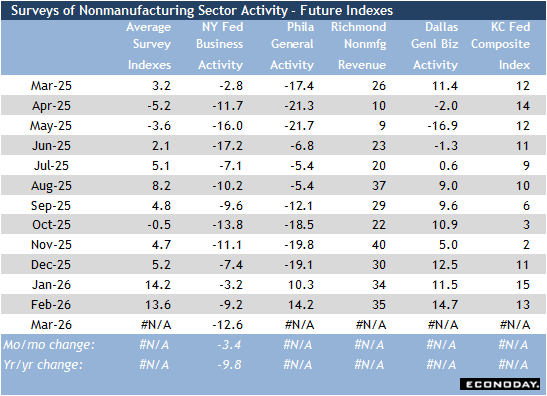

Also worth noting is that direction of the indexes for

future business conditions. Weakening expectations for growth have implications

for hiring and investing that drag on the economy. This probably isn't steep

enough to raise concerns about a recession, but the economy keeps getting hit

with headwinds like the chaos of trade and tariff policy, massive government

layoffs, and now oil prices on top of already troubling geopolitical

situations.

Now that the FOMC meeting and its attendant communications

blackout period are past, it is possible a date for Fed Chair Jerome Powell's

semiannual monetary policy testimony will finally be scheduled. However,

Congress's district work weeks begins on Wednesday, April 1 and runs through

Friday, April 10. There is almost no opportunity for it to take place before

then.

The Week Ahead: Econoday Consensus Forecasts

Monday

Singapore CPI for February (Mon 1300 CST; Mon 0500

GMT; Mon 0100 EDT)

Consensus Forecast, Y/Y: 1.2%

Consensus Range, Y/Y: 1.2% to 1.7%

The consensus sees annual inflation down to 1.2 percent in

February from 1.4 percent in January.

US Construction Spending for January (Mon 1000 EDT;

Mon 1400 GMT)

Consensus Forecast, M/M: 0.3%

Consensus Range, M/M: 0.1% to 0.7%

Spending is seen up 0.3 percent in January on month after

rising by the same 0.3 percent in December.

Eurozone EC Consumer Confidence Flash for March (Mon

1600 CET; Mon 1500 GMT; Mon 1100 EDT)

Consensus Forecast, Index: -14.5

Consensus Range, Index: -17 to -12.2

The consensus looks for consumer confidence down at minus

14.5 versus minus 12.2 in February with fallout from rising energy prices.

Tuesday

Japan CPI for October (Tue 0830 JST; Mon 2330 GMT; Mon

1930 EDT)

Consensus Forecast, CPI - Y/Y: 1.5%

Consensus Range, CPI - Y/Y: 1.3% to 1.5%

Consensus Forecast, Ex-Fresh Food - Y/Y: 1.7%

Consensus Range, Ex-Fresh Food - Y/Y: 1.6% to 1.8%

Consensus Forecast, Ex-Fresh Food & Energy - Y/Y:

2.7%

Consensus Range, Ex-Fresh Food & Energy - Y/Y: 2.6%

to 3.0%

Japan's nationwide core consumer price index is expected to

decelerate to its lowest level in nearly four years in February, slowing for

the third straight month, driven by lower energy prices and the government's

measures to curb utility costs, in line with the trend seen in Tokyo late last

month. Still, the underlying uptrend in consumer inflation remains intact amid

continued strength in overall food prices, although they have shown signs of

easing in recent months.

The core CPI, which excludes fresh food, is seen rising 1.7

percent on the year in February after a 2.0 percent increase a month earlier.

Core inflation is set to fall below the Bank of Japan's 2.0 percent target for

the first time since March 2022, marking its lowest level in almost four years.

This also represents a sharp slowdown from 3.0 percent recorded in October and

November.

Two other key measures are expected to be little changed to

slightly higher. Total CPI is projected to be unchanged, rising 1.5 percent on

the year in February, the same pace as a month earlier. The core-core CPI,

which excludes both fresh food and energy, is seen inching up to 2.7 percent

from 2.6 percent in January.

Eurozone PMI Composite Flash for March (Tue 0900 CET;

Tue 0800 GMT; Tue 0400 EDT)

Consensus Forecast, Composite Index: 50.7

Consensus Range, Composite Index: 50.0 to 52.0

Consensus Forecast, Manufacturing Index: 49.7

Consensus Range, Manufacturing Index: 49.0 to 51.5

Consensus Forecast, Services Index: 50.8

Consensus Range, Services Index: 50.0 to 52.0

The consensus sees the PMI composite flash stalling a bit at

50.7 in March versus 51.9 in the February final. Manufacturing PMI is seen at 49.7

in the March flash versus 50.8 in February final. The services PMI is seen at 50.8

in the March flash versus 51.9 in February final.

Germany PMI Composite Flash for March (Tue 0930 CET; Tue

0830 GMT; Tue 0430 EDT)

Consensus Forecast, Composite Index: 52.0

Consensus Range, Composite Index: 52.0 to 52.1

Consensus Forecast, Manufacturing Index: 49.5

Consensus Range, Manufacturing Index: 49.0 to 50.7

Consensus Forecast, Services Index: 52.4

Consensus Range, Services Index: 51.5 to 52.8

The consensus sees the PMI composite flash at 52.0 in March

versus 53.2 in the February final. Manufacturing PMI is seen at 49.5 in March

flash versus 50.9 in February final. The services PMI is seen at 52.4 in the

March flash versus 53.5 in February final.

UK PMI Composite Flash for March (Tue 0930 GMT; Tue 0530

EDT)

Consensus Forecast, Manufacturing Index: 51.0

Consensus Range, Manufacturing Index: 51.0 to 51.1

Consensus Forecast, Services Index: 53.0

Consensus Range, Services Index: 51.8 to 53.5

Manufacturing PMI is seen down to marginal growth 51.0 in the

March flash versus 51.6 in the February final.

US Productivity and Costs for Fourth Quarter - Final

Revision (Tue 0830 EDT; Tue 1230 GMT)

Consensus Forecast, Nonfarm Productivity - Annual Rate:

2.4%

Consensus Range, Nonfarm Productivity - Annual Rate: 2.0%

to 2.8%

Consensus Forecast, Unit Labor Costs - Annual Rate: 3.0%

Consensus Range, Unit Labor Costs - Annual Rate: 2.2%

to 3.4%

The consensus sees productivity growth revised down to 2.4

percent from 2.8 percent previously reported for the final Q4 figure. Unit

labor costs is expected to be revised up to 3.0 percent from 2.8 percent.

US PMI Composite Flash for March (Tue 0945 EDT; Tue 1345

GMT)

Consensus Forecast, Manufacturing Index: 51.0

Consensus Range, Manufacturing Index: 50.2 to 51.2

Manufacturing PMI expected down at 51.0 in March flash from

52.4 in the February final.

Wednesday

Australia Monthly CPI for February (Wed 1130 AET; Wed

0030 GMT; Tue 2030 EDT)

Consensus Forecast, Y/Y: 3.8%

Consensus Range, Y/Y: 3.5% to 4.3%

No change expected in CPI at 3.8 percent on year.

UK CPI for February (Wed 0700 GMT; Wed 0300 EDT)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: 0.2% to 0.5%

Consensus Forecast, Y/Y: 3.0%

Consensus Range, Y/Y: 2.8% to 3.1%

CPI expected up 0.4 percent on the month and 3.0 percent on

year in February after declining by 0.5 percent on the month in and the same

3.0 percent on year in January.

Germany Ifo Survey for March (Tue 1000 CET; Tue 0900

GMT; Tue 0500 EDT)

Consensus Forecast, Business Climate: 86.8

Consensus Range, Business Climate: 84.9 to 88.2

Consensus Forecast, Current Conditions: 86.4

Consensus Range, Current Conditions: 86.0 to 87.2

Consensus Forecast, Business Expectations: 88.0

Consensus Range, Business Expectations: 87.0 to 90.5

Erosion in confidence expected with the business climate

index down to 86.8 in March from 88.6 in February.

Thursday

Singapore Industrial Production for February (Thu

1300 CST; Thu 0500 GMT; Thu 0100 EDT)

Consensus Forecast, Y/Y: 14.1%

Consensus Range, Y/Y: 10.0% to 14.3%

Another strong gain is the call for February -- 14.1 percent

on year after 16.6 percent in January.

Norway Norges Bank Rate Decision (Thu 0800 CET; Thu 0700

GMT; Thu 0300 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 4.00%

Consensus Range, Level: 4.00% to 4.00%

Everyone expects the Norges Bank to stay on hold this time

but guidance will suggest rate hikes are coming as price pressures multiply.

Germany GfK Consumer Climate for April (Thu 0800 CET;

Thu 0700 GMT; Thu 0300 EDT)

Consensus Forecast, Index: -28.0

Consensus Range, Index: -29.5 to -25.6

As in the Ifo, consumers are gloomier. The consensus sees

Gfk index down at minus 28.0 in April from minus 24.7 in March.

Eurozone M3 Money Supply for February (Thu 1000 CET;

Thu 0900 GMT; Thu 0500 EDT)

Consensus Forecast, Y/Y-3-Month Moving Average: 3.4%

Consensus Range, Y/Y-3-Month Moving Average: 3.1% to 3.4%

Expected a little stronger at 3.4 percent for February after

3.0 percent in January.

US Jobless Claims for Week03/21 (Thu 0830 EDT; Thu 1230

GMT)

Consensus Forecast, Initial Claims - Level: 210K

Consensus Range, Initial Claims - Level: 207K to 215K

Claims seen at 210K, closer to the 4-week moving average of

210.75K, up from 205K last week.

Friday

UK Retail Sales for February (Fri 0700 GMT; Fri 0300

EDT)

Consensus Forecast, M/M: 0.1%

Consensus Range, M/M: -0.4% to 0.2%

Consensus Forecast, Y/Y: 2.4%

Consensus Range, Y/Y: 1.8% to 3.8%

The consensus sees sales up 0.1 percent on the month and 2.4

percent on year for February.

US Consumer Sentiment for March - Final (Fri 1000 EDT;

Fri 1400 GMT)

Consensus Forecast, Index: 54.3

Consensus Range, Index: 53.0 to 55.5

The consensus looks for sentiment to be revised down to 54.3

in the final March report from 55.5 in the preliminary March reading due largely

to rising energy prices flowing from the Iran war.

|