|

The Week Ahead: Highlights

Asia-Pacific Preview

Purchasing Managers Reports Ahead

By Brian Jackson, Econoday Economist

PMI surveys for March will be the main focus in the

Asia-Pacific region. The Flash PMI survey for India released last week showed

some moderation in conditions, and the fullest of surveys next week will be

watched for early signs that the Iran conflict has impacted activity and

sentiment in the region.

The minutes of the Reserve Bank of Australia's March meeting will be published in

the week ahead and may provide more insight into the decision to raise rates at

that meeting and guidance on whether more rate increases are likely in coming

months. Australian trade data for February are scheduled for release, as are

inflation, industrial production and retail sales data for South Korea. The

South Korean data will be followed by the Bank of Korea's next policy meeting

the following week.

Europe Preview

European Inflation's Moment of Truth

By Marco Babic, Econoday Economist

The week ahead sees the release of flash inflation data for

Europe's major economies for March which will show the impact of the conflict

in the Middle East. Recent rate decisions and policy announcements from central

banks in Europe have addressed the impact, and all are expecting inflation to

pick up. To be sure, European economies are protected somewhat from surging oil

prices due to the strength of the euro and Swiss franc against the dollar.

While price increases are clearly unwelcome and cut into consumer spending, the

main issue is that of supply and how that could be a factor for energy

production.

There had been some green shoots of optimism that order

books will recover in the coming year, particularly in France, which led to

investment in workers. That optimism given current development looks to be

misplaced.

Enter the Central Banks

Inflation has been relatively tame for at least the past

year in Europe, with that in most economies within the comfort zone of central

banks. Germany's CPI in February grew 0.2 percent month-on- month and 1.9

percent year-on-year. Italy's was up 0.7 percent and 1.5 percent month on

month, with France at 0.6 percent and 0.9 percent.

Even if hostilities ended tomorrow, there will be an impact

on inflation since, historically, prices don't climb down as quickly as they

rose. Furthermore, there is likely to be more risk built into prices and the

conflict has upended the perceived stability of the Gulf States.

For the central banks, inflation is one issue they are

mandated to keep under control. The second issue is that a global economic

slowdown, which the Swiss National Bank has cautioned about, increases the risk

of stagflation which is a harder dragon to slay that just inflation or economic

slowdown.

The upcoming data are likely to push the year-over-year

inflation rates towards or above 2.0 percent central bank inflation target in

the coming months. While core measures that exclude energy will no doubt show a

tamer inflation scenario, the fact remains that energy prices affect everyday

life.

US Preview

Jobs Data in Focus

By Theresa Sheehan, Econoday Economist

The focus of the March 30 week's data will be conditions in

the labor market. The story is expected to be the same as in recent months -

low hire and no fire.

The ADP report on private payrolls shows the four-week

moving average at an increase of 10,000 per week as of the March 7 week,

essentially unchanged from the average of 9,000 in the February 28 week and

slower than the average of 14,750 in the February 21 week and 15,500 in the

February 14 week. This points to slowing momentum in new hiring going into

March. Businesses are exercising caution about bringing on new employees as

well as having trouble finding workers with the right skills and/or experience.

However, they are also not cutting payrolls, at least not yet. The ADP national

employment report for the month of March is set for release at 8:15 ET on

Wednesday.

The Challenger report on job cut intentions for March is at

7:30 ET on Thursday. The February report showed a sharp decline of 55.5 percent

to 48,307 in February after a jump of 205.0 percent in January to 108,435 from

December. Employers probably made their biggest job cut decisions in the

post-holiday period with the elimination of planned new hires rather than

reducing existing payrolls. March should see the pace of planned job cut

actions level off and remain mostly in narrow industries where adoption of AI

tools is having the biggest impact.

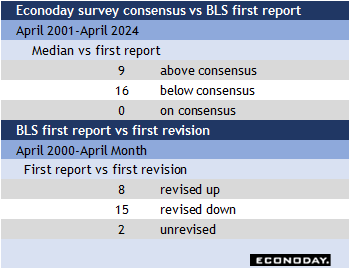

The BLS's monthly report on the employment situation for

March at 8:30 ET on Friday is expected to retrace at least some of the decline

of 92,000 in February that was largely due to special factors. Strikes by

healthcare workers have been settled and over 40,000 will be back on the job

and receiving paychecks. March should see anemic payrolls growth in the private

sector as only a few narrow sectors continue to hire. The first report of

payrolls in March tends to come in below consensus in part because of the

mid-month holiday in February that can slow data collection. However, the March

payroll numbers also have a strong tendency to subsequently be revised lower.

The Week Ahead: Econoday Consensus Forecasts

Monday

India Industrial Production for February (Tue 0850

JST; Mon 2350 GMT; Mon 1950 EDT)

Consensus Forecast, Y/Y: 4.3%

Consensus Range, Y/Y: 3.8% to 5.4%

Output expected up 4.3 percent on year in February versus

4.8 percent in January.

Germany CPI for March (Mon 1400 CEST; Mon 1200 GMT;

Mon 0800 EDT)

Consensus Forecast, M/M: 1.0%

Consensus Range, M/M: 1.0% to 1.2%

Consensus Forecast, Y/Y: 2.6%

Consensus Range, Y/Y: 2.6% to 3.0%

CPI expected to show increases of 1.0 percent on month and 2.6

percent on year versus 0.2 percent and 1.9 percent in February as the oil shock

effect arrives.

Tuesday

Japan Tokyo CPI for March (Tue 0830 JST; Mon 2330

GMT; Mon 1930 EDT)

Consensus Forecast, CPI - Y/Y: 1.6%

Consensus Range, CPI - Y/Y: 1.4% to 1.6%

Consensus Forecast, Ex-Fresh Food - Y/Y: 1.8%

Consensus Range, Ex-Fresh Food - Y/Y: 1.6% to 1.9%

Consensus Forecast, Ex-Fresh Food & Energy - Y/Y:

2.4%

Consensus Range, Ex-Fresh Food & Energy - Y/Y: 2.2%

to 2.5%

Retail prices at supermarkets in early March showed a

deceleration trend, while

gasoline prices rose in mid-March amid worsening tensions in

the Middle East.

Still, the impact of the Middle East situation appears

limited, keeping the Tokyo core

CPI, which excludes fresh food, below the BOJ's inflation

target of 2 percent for the second

straight month. The core CPI is expected to be flat at a

rise of 1.8 percent on the year in

March after hitting a 16-month low of 1.8 percent in

February.

Elsewhere, the total CPI is expected to be unchanged at 1.6

percent on the year in March

from a month earlier. The core-core index, which excludes

fresh food and energy, is

seen slowing to a 2.4 percent rise from 2.5 percent in

February.

Japan Unemployment Rate for February (Tue 0830 JST; Mon

2330 GMT; Mon 1930 EDT)

Consensus Forecast, Rate: 2.7%

Consensus Range, Rate: 2.6% to 2.7%

Japan's seasonally adjusted unemployment rate is seen

holding steady at 2.7 percent in February, reflecting continuing labor shortage

across a wide range of industries. Last month, the unemployment rate edged up

to 2.7 percent to the highest level since July 2024 and payroll unexpectedly

fell on the year for the first time in 42 months.

The number of employed persons in January dropped 30,000 to

67.76 million, marking the first decline in 42 months. Meanwhile, the number of

unemployed persons rose to 1.79 million, up 160,000 on the year, marking the

sixth consecutive monthly increase.

Japan Industrial Production for February (Tue 0850

JST; Mon 2350 GMT; Mon 1950 EDT)

Consensus Forecast, M/M: -2.0%

Consensus Range, M/M: -3.5% to -0.5%

Consensus Forecast, Y/Y: 0.4%

Consensus Range, Y/Y: -1.2% to 1.9%

Japan's industrial production is expected to fall sharply on

the month in February, marking its first decline in three months as exports

slow following front-loaded activity ahead of the Lunar New Year that boosted

output in the previous month.

Output is seen falling 2.0 percent on the month in February

after a revised 4.3 percent rise in January, which was up from an initial 2.2

percent increase. The January rebound was also reflected in a surge in exports

of computer chips, non-ferrous metals and plastics ahead of holidays in China

and other parts of Asia around the Feb. 17 Lunar New Year.

On a year-on-year basis, production is expected to rise 0.4

percent in February, compared with a revised 0.7 percent increase from an

originally reported 2.3 percent gain in January.

China CFLP Composite PMI for March (Tue 0930 CST; Tue

0130 GMT; Mon 2130 EDT)

Consensus Forecast, Manufacturing Index: 49.9

Consensus Range, Manufacturing Index: 49.8 to 50.2

Manufacturing business seen better at 50.2 in March versus

49.0 in February.

UK GDP for Fourth Quarter (Tue 0700 GMT; Tue 0200 EDT)

Consensus Forecast, Q/Q: 0.1%

Consensus Range, Q/Q: 0.1% to 0.1%

Consensus Forecast, Y/Y: 1.0%

Consensus Range, Y/Y: 1.0% to 1.0%

Growth rate expected unrevised at 0.1 percent on quarter and

1.0 percent on year for the final Q4 reading.

Germany Unemployment Rate for March (Tue 0955 CEST; Tue

0755 GMT; Tue 0355 EDT)

Consensus Forecast, Rate: 6.3%

Consensus Range, Rate: 6.3% to 6.3%

Rate seen stuck again at 6.3 percent in March.

Eurozone HICP Flash for March (Tue 1100 CEST; Tue 0900

GMT; Tue 0500 EDT)

Consensus Forecast, HICP - Y/Y: 2.7%

Consensus Range, HICP - Y/Y: 2.2% to 3.1%

Consensus Forecast, Narrow Core - Y/Y: 2.4%

Consensus Range, Narrow Core - Y/Y: 2.3% to 2.7%

Oil price surge driving consumer prices up, expected at 2.7

percent in March versus 1.9 percent in the February final. This is what the ECB

President Christine Lagarde was talking about when she threatened rate hikes.

Canada Monthly GDP for January (Tue 0830 EDT; Tue

1230 GMT)

Consensus Forecast, M/M: 0.0%

Consensus Range, M/M: 0.0% to 0.0%

Forecasters agree with StatsCan's advance estimate that

looks for GDP flat in January after 0.2 percent growth in December. That

reflects manufacturing plant outages offset by gains in energy sector output.

US Chicago PMI for March (Tue 0945 EDT; Tue 1345 GMT)

Consensus Forecast, Index: 54.0

Consensus Range, Index: 52.0 to 55.1

After an amazing pop into positive territory at 57.7 in

February, the consensus sees March holding strong at 54.0. After years of

contraction, this is hard to fathom.

US Consumer Confidence for March (Tue 1000 EDT; Tue 1400

GMT)

Consensus Forecast, Index: 88.5

Consensus Range, Index: 86.0 to 89.5

The consensus sees confidence down at 88.5 in March versus

91.1 in February and 89.0 in January. Worries about inflation and jobs continue

to weigh and the Iran war is darkening the picture for consumers.

Wednesday

Japan Tankan for First Quarter (Wed 0850 JST; Tue

2350 GMT; Tue 1950 EDT)

Consensus Forecast, Large Manufacturer Sentiment Index:

17

Consensus Range, Large Manufacturer Sentiment

Index: 8 to 18

Consensus Forecast, Large Non-Manufacturer Sentiment

Index: 34

Consensus Range, Large Non-Manufacturer Sentiment Index:

28 to 35

Consensus Forecast, Small Manufacturer Sentiment Index:

7

Consensus Range, Small Manufacturer Sentiment

Index: -1 to 9

Consensus Forecast, Small Non-Manufacturer Sentiment

Index: 14

Consensus Range, Small Non-Manufacturer Sentiment Index:

8 to 16

FY Current, 2025

Consensus Forecast, Large Firms Capital Expenditure Plans:

9.7%

Consensus Range, Large Firms Capital Expenditure Plans:

9.0% to 11.4%

Consensus Forecast, Small Firms Capital Expenditure Plans:

-0.6%

Consensus Range, Small Firms Capital Expenditure Plans:

-2.9% to 4.4%

The Bank of Japan's quarterly Tankan business sentiment

survey is expected to show a slight improvement among large manufacturers in

the March quarter, while the recent plunge in the number of Chinese tourists

amid bilateral diplomatic rows is seen weighing on sentiment among both large

and small non-manufacturers.

U.S. and Israeli attacks on Iran appear to have had only a

limited immediate impact on Japanese corporate sentiment. Still, concerns about

the outlook are intensifying, prompting firms to remain cautious on capital

spending as volatile global oil prices and rising domestic energy costs add to

uncertainty.

Against this backdrop, the March Tankan diffusion index for

large manufacturers is projected at 17, edging up from a revised 16, previously

15, in December and marking a fourth straight quarterly increase. The index for

small manufacturers is expected to be unchanged at 7, compared with a revised

7, previously 6.

China PMI Manufacturing for March (Wed 0945 CST; Wed

0145 GMT; Tue 2045 EDT)

Consensus Forecast, Index: 52.5

Consensus Range, Index: 51.7 to 53.0

The index is seen at 52.5 in March versus 52.1 in February.

Eurozone Unemployment Rate for February (Wed 1100 CEST;

Wed 0900 GMT; Wed 0400 EDT)

Consensus Forecast, Rate: 6.1%

Consensus Range, Rate: 6.1% to 6.2%

No change from 6.1 percent is the call.

US Retail Sales for February (Wed 0830 EDT; Wed 1230

GMT)

Consensus Forecast, Retail Sales - M/M: 0.4%

Consensus Range, Retail Sales - M/M: -0.1% to 1.0%

Consensus Forecast, Ex-Vehicles - M/M: 0.3%

Consensus Range, Ex-Vehicles - M/M: -0.1% to 0.4%

Consensus Forecast, Ex-Vehicles & Gas - M/M: 0.2%

Consensus Range, Ex-Vehicles & Gas - M/M: 0.2% to

0.3%

The consensus looks for retail sales up 0.4 percent in

February with sales ex-autos up 0. percent.

US ADP Employment for March (Wed 0815 EDT; Wed 1315

GMT)

Consensus Forecast, Jobs: 40K

Consensus Range, Jobs: 30K to 50K

The weekly ADP report has been showing jobs up 10K a week on

average in March, so that means about 40K a month.

US PMI Manufacturing Final for March (Wed 0945 EDT; Wed

1345 GMT)

Consensus Forecast, Index: 52.4

Consensus Range, Index: 52.1 to 53.5

No revision expected from the flash at 52.4.

US ISM Manufacturing Index for March (Wed 1000 EDT; Wed

1400 GMT)

Consensus Forecast, Index: 52.3

Consensus Range, Index: 52.0 to 53.0

The consensus sees the index pretty steady at 52.3 in March

vs. 52.4 in February, suggesting modest growth.

Thursday

South Korea CPI for March (Thu 0800 KST; Wed 2300

GMT; Wed 1900 EDT)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: 0.1% to 0.6%

Consensus Forecast, Y/Y: 2.2%

Consensus Range, Y/Y: 1.5% to 3.5%

The consensus looks for CPI up 0.2 percent on month and 2.2

percent on year for March after 0.3 percent and 2.0 percent in February.

Australia International Trade in Goods for October (Thu

1130 AEDT; Thu 0030 GMT; Wed 2030 EDT)

Consensus Forecast, Balance: A$2.7 B

Consensus Range, Balance: A$1.5 B to A$3.5 B

The surplus is seen stable at A$2.7 billion in February

versus A$2.631 billion in January.

Canada Merchandise Trade for February (Thu 0830 EDT;

Thu 1230 GMT)

Consensus Forecast, Balance: -C$1.8 B

Consensus Range, Balance: -4.8C$ B to -C$1.5 B

The consensus sees the deficit narrower at C$1.8 billion for

February versus a large deficit of C$3.649 billion in January on higher oil

prices and rising auto exports.

US International Trade in Goods and Services for February

(Thu 0830 EDT; Thu 1230 GMT)

Consensus Forecast, Balance: -$60.1 B

Consensus Range, Balance: -$68.7 B to -$45.0 B

The trade gap is expected a bit wider at $60.1 billion in

February from $54.5 billion in January. This one is hard to forecast given

tariff effects.

US Jobless Claims for Week 03/28 (Thu 0830 EDT; Thu 1230

GMT)

Consensus Forecast, Initial Claims - Level: 213K

Consensus Range, Initial Claims - Level: 197K to 220K

Claims are seen up at 213K versus 210K in the previous week.

Friday

China PMI Composite for March (Fri 0945 CST; Fri 0145

GMT; Thu 2145 EDT)

Consensus Forecast, Services Index: 53.7

Consensus Range, Services Index: 53.5 to 54.5

Services seen down at 53.7 in March versus 56.7 in February.

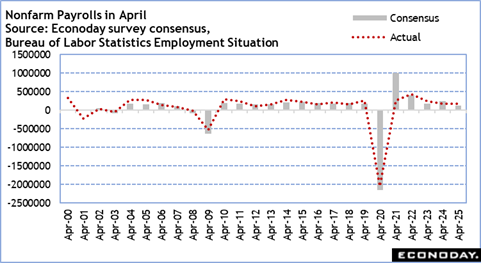

US Employment Situation for March (Fri 0830 EDT; Fri

1230 GMT)

Consensus Forecast, Nonfarm Payrolls - M/M: 51K

Consensus Range, Nonfarm Payrolls - M/M: -25K to 75K

Consensus Forecast, Unemployment Rate: 4.4%

Consensus Range, Unemployment Rate: 4.4% to 4.5%

Consensus Forecast, Private Payrolls - M/M: 56K

Consensus Range, Private Payrolls - M/M: 30K to 70K

Consensus Forecast, Average Hourly Earnings - M/M: 0.3%

Consensus Range, Average Hourly Earnings - M/M: 0.2%

to 0.4%

Consensus Forecast, Average Hourly Earnings - Y/Y: 3.8%

Consensus Range, Average Hourly Earnings - Y/Y: 3.6%

to 3.8%

Consensus Forecast, Average Workweek: 34.3

Consensus Range, Average Workweek: 34.3 to 34.3

Payrolls seen back up by 51K after a surprise drop of 92K in

February. Jobless rate expected flat at 4.4 percent in March versus 4.4 percent

in February. Earnings growth expected at 0.3 percent, down from 0.4 percent in

February.

|