|

The Week Ahead: Highlights

US Preview

CPI Report, Energy Price Shock Effects Key for Fed Policy

Outlook

By Theresa Sheehan, Econoday Economist

The April 6 week has a light data report schedule and only

one report that is likely to prove significant. Much of the data on the

schedule predates the war on Iran begun on February 28. Data that covers the

period immediately after will not offer clarity about the war's impact on the

US as it is unknown how long the war will last or if its impact has been deep

enough to have more than a short-term effect.

With the April 28-29 FOMC meeting on the near horizon, the

focus will be on data that has implications for Fed monetary policy. Now that

the March employment report is out of the way, risks to the maximum employment

side of the Fed's dual mandate are better understood. The labor market appears

to be holding on to is "low hire, no fire" trend. Labor supply and demand

appear to be in an equilibrium that could easily tip towards weaker conditions

but is not in imminent danger of doing so.

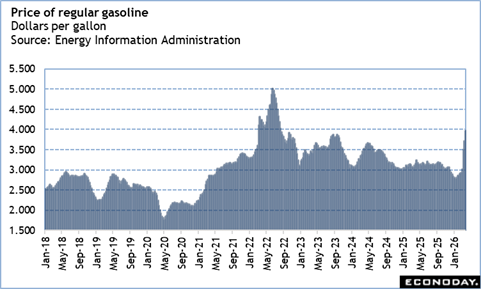

The risks to price stability should be more evident in the

March consumer price index (CPI) numbers at 8:30 ET on Friday. The one

immediately visible effect of the war on Iran will be in energy prices. The

cost of a gallon of regular gasoline jumped about $1 between February and

March. Other consumer prices will be slower to react, if at all. At least some

commodities prices like imported foods are going to move higher, but it will

take time for it to pass through from the wholesale level. The steep price climb

for energy is going to meaningfully cut into consumer discretionary spending in

March, raise short-term inflation expectations, and be another setback in

bringing inflation back to the Fed's 2 percent objective.

Just at the time the 2025 hikes in tariffs were exiting the

inflation data, the inflation measures will reflect a boost in commodity prices

and probably an increase for services as well as businesses impose fees to

cover their costs. While the blow from suddenly higher energy prices is likely

to be a one-off, if higher prices linger, these will be a drag on growth.

The release of the FOMC meeting minutes of March 17-18 at

14:00 ET on Wednesday is not expected to provide any useful insights about the

upcoming FOMC meeting. The March deliberations took place at a time of great

uncertainty in the first weeks after the war started and that uncertainty has

yet to resolve amid chaotic messaging out of the White House and geopolitical

developments.

There is still no scheduled date for Fed Chair Jerome

Powell's semiannual monetary policy testimony and will not be until after

Congress returns from its spring work period (March 30-April 10). The Senate

Banking Committee has yet to schedule a confirmation hearing for Fed governor

and chair nominee Kevin Warsh.

The Week Ahead: Econoday Consensus Forecasts

Monday

India PMI Composite Flash for March (Mon 1030 IST;

Mon 0500 GMT; Mon 0100 EDT)

Consensus Forecast, Composite Index: 56.5

Consensus Range, Composite Index: 56.5 to 56.5

Consensus Forecast, Services Index: 57.2

Consensus Range, Services Index: 57.2 to 57.2

The consensus sees no revision from the flash at 56.5 for

composite and 57.2 for services for the March final. That is down from 58.9 and

58.1, respectively, in February final.

US ISM Services Index for March (Mon 1000 EDT; Tue 1400

GMT)

Consensus Forecast, Index: 54.7

Consensus Range, Index: 53.0 to 55.5

The services PMI is seen a bit slower but still showing

growth at 54.7 in March after surging to 56.1 in February from 53.8 in January.

Services continue to expand nicely though price pressures threaten to spoil the

party.

Tuesday

Japan Household Spending for February (Tue 0830 JST; Mon

2330 GMT; Mon 1930 EDT)

Consensus Forecast, M/M: 2.3%

Consensus Range, M/M: -0.9% to 3.9%

Consensus Forecast, Y/Y: -0.8%

Consensus Range, Y/Y: -2.9% to 0.5%

Japan's real household spending is expected to fall year

over year for a third consecutive month in February amid signs of a broad

slowdown in department store and supermarket sales, as well as declines in new

passenger car registrations. The trend is underscored by February retail sales

data, which posted the first year-over-year decline in two months.

Household spending in February is expected to fall 0.8

percent from a year earlier after a 1.0 percent decline in January. The January

drop was driven by a 10th consecutive year-on-year decline in both gift-related

spending and mobile communication charges, as well as volatility in private

university tuition fees.

Still, household spending is expected to rise on a monthly

basis for the first time in three months, increasing 2.3 percent month-on-month

in February after slipping 2.0 percent in January.

Australia Household Spending for February (Tue 1130

AEST; Tue 0130 GMT; Mon 2130 EDT)

Consensus Forecast, M/M: -0.2%

Consensus Range, M/M: -0.2% to 0.4%

The consensus sees spending down 0.2 percent in February,

reflecting falling credit card spending. This decline is appearing well before

the effect of higher fuel prices starting in March -- expected to have a huge

disruptive effect on sales ex-fuel.

France PMI Composite Final for March (Tue 0850 CEST; Tue

0650 GMT; Tue 0250 EDT)

Consensus Forecast, Services Index: 48.3

Consensus Range, Services Index: 48.3 to 48.3

The consensus sees no revision in the final services index

from the flash at 48.3 for March versus 49.6 in February.

Eurozone PMI Composite Final for March (Tue 0900 CEST;

Tue 0700 GMT; Tue 0300 EDT)

Consensus Forecast, Composite Index: 50.5

Consensus Range, Composite Index: 50.5 to 50.5

Consensus Forecast, Services Index: 50.1

Consensus Range, Services Index: 50.1 to 50.1

The consensus sees no revision in the final composite index

from the flash at 50.5 for March versus 51.9 in February. The consensus also

sees no revision in the final services index from the flash at 50.1 for March

versus 51.9 in February

Germany PMI Composite Final for March (Tue 0955 CEST;

Tue 0755 GMT; Tue 0355 EDT)

Consensus Forecast, Composite Index: 51.9

Consensus Range, Composite Index: 51.9 to 51.9

Consensus Forecast, Services Index: 51.2

Consensus Range, Services Index: 51.2 to 51.2

The consensus sees no revision in the final composite index

from the flash at 51.9 for March versus 53.2 in February. The consensus also

sees no revision in the final services index from the flash at 51.2 for March

versus 53.5 in February.

UK PMI Composite Final for March (Tue 0930 GMT; Tue 0530

EDT)

Consensus Forecast, Composite Index: 51.0

Consensus Range, Composite Index: 50.7 to 51.0

Consensus Forecast, Services Index: 51.2

Consensus Range, Services Index: 51.2 to 51.2

The consensus sees no revision in the final composite index

from the flash at 51.0 for March versus 53.7 in February. The consensus also

sees no revision in the final services index from the flash at 51.2 for March

versus 53.9 in February.

US Durable Goods Orders for February (Tue 0830 EDT;

Tue 1230 GMT)

Consensus Forecast, New Orders - M/M: -0.2%

Consensus Range, New Orders - M/M: -4.5% to 2.0%

Consensus Forecast, Ex-Transportation - M/M: 0.7%

Consensus Range, Ex-Transportation - M/M: 0.6% to 0.7%

Consensus Forecast, Core Capital Goods - M/M: 0.3%

Consensus Range, Core Capital Goods - M/M: 0.3% to 0.4%

Forecasters see a drop in aircraft orders leading to a 0.2

percent decline in total durable goods orders with an uptick of 0.7% in orders

ex-transportation. Non-defense capital goods orders are also seen up by 0.3

percent with AI-related capex leading the way.

US Consumer Credit for February (Tue 1500 EDT; Tue 1100

GMT)

Consensus Forecast, M/M: $12.0 B

Consensus Range, M/M: $2.0 B to $14.0 B

The consensus sees credit up by a moderate $12 billion for

February after rising $8.1 billion in January.

Wednesday

New Zealand RBNZ Announcement (Wed 1400 NZDT; Wed

0100 GMT; Tue 2200 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 2.25%

Consensus Range, Level: 2.25% to 2.25%

The consensus sees the RBNZ leaving rates steady. Attention

will focus on what the bank has to say about the impact of rising energy prices

and disruptions to growth flowing from the Mideast conflict.

India Reserve Bank of India Announcement (Wed 1000

IST; Wed 0430 GMT; Wed 0030 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 5.25%

Consensus Range, Level: 5.25% to 5.25%

Analysts expect the RBI to leave rates on hold for now

awaiting the impact of rising energy prices on growth and inflation.

Germany Manufacturing Orders for February (Wed 0800

CEST; Wed 0600 GMT; Wed 0200 EDT)

Consensus Forecast, M/M: 2.5%

Consensus Range, M/M: 1.0% to 8.0%

Consensus Forecast, Y/Y: 5.0%

Consensus Range, Y/Y: 5.0% to 5.5%

Orders expected to rebound by 2.5 percent on the month in

February after plunging by 11.1 percent in January. On year, sales seen up 5.0

percent after increasing 4.0 percent in January.

Switzerland Unemployment Rate for March (Wed 0900 CEST;

Wed 0700 GMT; Wed 0300 EDT)

Consensus Forecast, Adjusted: 3.0%

Consensus Range, Adjusted: 3.0% to 3.0%

No change seen at 3.0 percent.

Eurozone Retail Sales for February (Wed 1100 CEST; Wed

1000 GMT; Wed 0500 EDT)

Consensus Forecast, M/M: 0.0%

Consensus Range, M/M: -0.2% to 0.2%

Consensus Forecast, Y/Y: 1.8%

Consensus Range, Y/Y: 1.7% to 1.8%

The consensus sees sales flat on the month and up 1.8

percent on year in February after falling 0.1 percent on month and rising 2.0

percent on year in January.

Eurozone PPI for February (Wed 1100 CEST; Wed 1000

GMT; Wed 0500 EDT)

Consensus Forecast, M/M: -0.2%

Consensus Range, M/M: -0.3% to 0.5%

Consensus Forecast, Y/Y: -2.5%

Consensus Range, Y/Y: -3.2% to -1.9%

Wholesale prices under deflationary pressure with the

consensus looking for declines of 0.2 percent on month and 2.5 percent on year for

February.

Thursday

Germany Industrial Production for February (Thu 0800

CEST; Thu 0600 GMT; Thu 0200 EDT)

Consensus Forecast, M/M: 0.3%

Consensus Range, M/M: -1.0% to 1.5%

Consensus Forecast, Y/Y: 0.3%

Consensus Range, Y/Y: -1.0% to 1.0%

Output expected with sluggish with increases of 0.3 percent

on month and 0.3 percent on year for February.

Germany Merchandise Trade for February (Thu 0800 CEST;

Thu 0600 GMT; Thu 0200 EDT)

Consensus Forecast, Balance: E19.1 B

Consensus Range, Balance: E18.0 B to E19.1 B

The consensus sees the surplus down to E19.1 billion in

February from $21.2 billion in January.

US GDP for Fourth Quarter (Thu 0830 EDT; Thu 1230

GMT)

Consensus Forecast, Q/Q - Annual Rate: 0.7%

Consensus Range, Q/Q - Annual Rate: 0.6% to 1.4%

No revision expected in the growth rate at 0.7 percent in

the final Q4 report.

US Jobless Claims for Week04/04 (Thu 0830 EDT; Thu 1230

GMT)

Consensus Forecast, Initial Claims - Level: 213K

Consensus Range, Initial Claims - Level: 208K to 220K

Claims expected back up to 213K after falling by 9K to 202K

last week.

US Personal Income and Outlays for February (Thu 0830

EDT; Thu 1230 GMT)

Consensus Forecast, Personal Income - M/M: 0.4%

Consensus Range, Personal Income - M/M: 0.2% to 0.4%

Consensus Forecast, Personal Consumption Expenditures -

M/M: 0.5%

Consensus Range, Personal Consumption Expenditures - M/M:

0.1% to 0.6%

Consensus Forecast, PCE Price Index - M/M: 0.4%

Consensus Range, PCE Price Index - M/M: 0.3% to 0.4%

Consensus Forecast, PCE Price Index - Y/Y: 2.8%

Consensus Range, PCE Price Index - Y/Y: 2.7% to 2.9%

Consensus Forecast, Core PCE Price Index - M/M: 0.3%

Consensus Range, Core PCE Price Index - M/M: 0.2% to

0.4%

Consensus Forecast, Core PCE Price Index - Y/Y: 2.9%

Consensus Range, Core PCE Price Index - Y/Y: 2.8% to

3.1%

Forecasters look for a strong 0.4 percent increase in

personal income with a 0.5 percent rise in personal spending.

Friday

Japan PPI for March (Fri 0750 JST; Thu 2350 GMT; Thu

1950 EDT)

Consensus Forecast, M/M: 0.5%

Consensus Range, M/M: 0.2% to 2.1%

Consensus Forecast, Y/Y: 2.1%

Consensus Range, Y/Y: 0.8% to 3.8%

The CGPI is projected to rise 2.1 percent from a year

earlier in March, with the pace of increase ticking up from a nearly two-year

low of 2.0 percent in February. The annual rate would remain the lowest since

April 2024, when the CGPI rose 1.2 percent, and extend the streak of increases

to 61 consecutive months.

On a month-on-month basis, the CGPI is expected to rise 0.5

percent in March after slipping 0.1 percent in February.

South Korea Bank of Korea Announcement (Fri 1000 KST;

Fri 0100 GMT; Fri 2100 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 2.5%

Consensus Range, Level: 2.5% to 2.5%

The consensus looks for no change this time.

China CPI for March (Fri 0930 CET; Fri 0130 GMT; Thu

2130 EDT)

Consensus Forecast, Y/Y: 1.2%

Consensus Range, Y/Y: 1.1% to 1.5%

CPI expected down a bit at 1.2 percent on year in March from

1.3 percent in February.

China PPI for March (Fri 0930 CET; Fri 0130 GMT; Thu

2130 EDT)

Consensus Forecast, Y/Y: 0.5%

Consensus Range, Y/Y: -1.0% to 0.7%

The consensus sees the long-desired end to wholesale price deflation

with PPI up 0.5 percent on year in March versus minus 0.9 percent in February.

Germany CPI for March (Fri 0800 CEST; Fri 0600 GMT;

Fri 0200 EDT)

Consensus Forecast, M/M: 1.1%

Consensus Range, M/M: 1.1% to 1.2%

Consensus Forecast, Y/Y: 2.7%

Consensus Range, Y/Y: 2.7% to 2.7%

Consensus Forecast, HICP - M/M: 1.2%

Consensus Range, HICP - M/M: 1.2% to 1,2%

Consensus Forecast, HICP - Y/Y: 2.8%

Consensus Range, HICP - Y/Y: 2.8% to 2.8%

No revision expected from the flash with CPI seen up 1.1

percent on month, reflecting the energy price shock, and 2.7 percent on year.

Canada Labour Force Survey for March (Fri 0830 EDT;

Fri 1230 GMT)

Consensus Forecast, Employment - M/M: 18K

Consensus Range, Employment - M/M: 15K to 40K

Consensus Forecast, Unemployment Rate: 6.8%

Consensus Range, Unemployment Rate: 6.6% to 6.9%

After two months of big losses, employment is expected to

rebound by 18,000 for March but unemployment seen ticking up to 6.8 percent

from 6.7 percent.

US CPI for March (Fri 0830 EDT; Fri 1230 GMT)

Consensus Forecast, CPI - M/M: 0.9%

Consensus Range, CPI - M/M: 0.8% to 1.3%

Consensus Forecast, CPI - Y/Y: 3.4%

Consensus Range, CPI - Y/Y: 2.6% to 3.8%

Consensus Forecast, Ex-Food & Energy - M/M: 0.3%

Consensus Range, Ex-Food & Energy - M/M: 0.2% to 0.4%

Consensus Forecast, Ex-Food & Energy - Y/Y: 2.7%

Consensus Range, Ex-Food & Energy - Y/Y: 2.6% to 2.8%

The consensus sees CPI up a huge 0.9 percent on the month

and an uncomfortable 0.3 percent excluding food and energy. The consensus sees

CPI up 3.4 percent on year and 2.7 percent ex-food and energy. Retail gas

prices have been reported up 25 percent for March and everyone is watching to

see how much the energy shock spreads. These numbers keep the Fed on hold for

now and considering rate hikes if it persists.

US Consumer Sentiment for April (Fri 1000 EDT; Fri 1400

GMT)

Consensus Forecast, Index: 52.0

Consensus Range, Index: 50.0 to 52.9

The Iran war and soaring gas prices expected to depress

sentiment in the preliminary April reading to 52.0 from 53.3 in the March

final.

US Factory Orders for February (Fri 1000 EDT; Fri 1400

GMT)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: -0.2% to 0.5%

A moderate 0.4 percent increase on month is the call for

February after a 0.1 percent uptick in January.

|