|

The Week Ahead: Highlights

Asia-Pacific Preview

Chinese GDP, Australia's Jobs Report Ahead

By Brian Jackson, Econoday Economist

Chinese data will be the main highlight of the Asia-Pacific

data calendar with GDP data for the three months to March and monthly activity

data for March scheduled for release. These data may show some initial impact

from the Iran conflict and will complement previously published PMI survey data

that showed subdued conditions in March. The data may also be accompanied by

commentary from officials referring to the Iran conflict and may provide some

guidance on their policy response.

China will also publish trade data for March, as will

Singapore. Singapore will publish GDP data next week ahead of a scheduled

policy meeting.

After the Reserve Bank of Australia's decision to increase

policy rates last month, Australian labour market data will be another key focus.

Officials at that meeting noted that labour market conditions have tightened

recently, reinforcing their concerns about the inflation outlook. Business and

consumer confidence surveys for Australia will also be published next month and

will indicate the impact on sentiment of the RBA's latest rate hike.

Europe Preview

Will Final European CPI Figures Show Further

Acceleration?

By Marco Babic, Econoday Economist

In the week ahead in Europe, final CPI results are coming

for a number of countries, and also the overall figure for the Eurozone. In the

case of the latter, flash results showed consumer prices rising 2.5 percent

year-on-year in March after 1.9 percent in February. The core rate slowed to

2.3 percent from 2.4 percent the month before.

While the final readings often validate the flash estimate,

the results are of increased interest due to the situation in the Middle East.

A deviation from the flash readings of 0.2 percent or more would be notable

since it would show a rapid rate of inflation.

Eurostat will also report trade figures for February, but

they won't show the impact of the conflict until the March results are

reported. While the US tariffs were deemed illegal, the US administration is

seeking other ways to impose them, which will be contributing further

uncertainty.

Even if the current fragile cease fire holds, crude oil

shipments will still take some time to get back to levels where they were

before, adding further strain to oil-dependent economies.

ECB Minutes

The European Central Bank will release the minutes of its

last policy meeting. Already in the statement following their March gathering,

they cited the conflict in the Middle East as being inflationary and having the

potential to dampen growth.

Due out on Thursday, the minutes will possibly give some

further details into the position of the Governing Council.

In any case, there are real risks arising that the

combination of rising prices and slowing economic growth could usher in a new

period of stagflation.

US Preview

Beige Book in Focus for Early View of Energy Shock's

Effects

By Theresa Sheehan, Econoday Economist

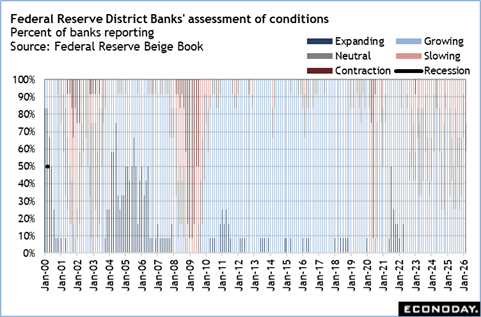

The most important report in the April 13 week may prove to

be the Fed's Beige Book at 14:00 ET on Wednesday. The contents will be

some of the most recent information about conditions across the 12 Federal

Reserve districts and will inform the decision on the next steps in monetary

policy at the FOMC meeting on April 28-29.

There were signs of softening in overall economic condition

in the prior report for the period of about early January through mid-February.

The upcoming report will cover roughly the period between late February through

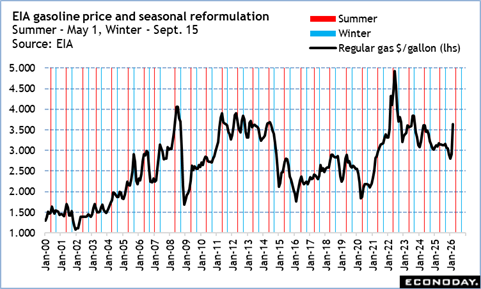

early April and will encompass the initial reactions to the economic shocks of

the war on Iran begun on February 28. This will include the surge in energy

prices and some immediate response where prices were hiked to cover higher

costs, such as in the transportation sector. The report will also encapsulate

conditions in the labor market and for wage pressures. The labor market is

expected to look soft, but stable. Wage gains should still be present, if

somewhat less, except for skilled workers in high demand like in the healthcare

sector.

The March report for the final-demand PPI is at 8:30 ET on

Tuesday and the import and export price indexes at 8:30 ET on Wednesday. These

will both reflect the same pressure from energy prices that hit commodities

costs in the March CPI report and which are likely to carry into April and

beyond for transportation services.

Congress returns from its spring working period on Monday.

It is possible there will be some movement in schedules the Fed chair's

semiannual monetary policy testimony and/or the nomination hearing for Kevin

Warsh as a Fed governor and its next chair.

The Week Ahead: Econoday Consensus Forecasts

Monday

US Existing Home Sales for March (Mon 1000 EDT; Mon 1400

GMT)

Consensus Forecast, Annual Rate: 4.08 M

Consensus Range, Annual Rate: 3.95 M to 4.18 M

Forecasters see sales nearly stable at an annual 4.08

million versus 4.09 million in February.

Tuesday

Singapore GDP for First Quarter (Tue 0800 SGT; Tue 0000

GMT; Mon 1900 EDT)

Consensus Forecast, Y/Y: 5.6%

Consensus Range, Y/Y: 5.0% to 6.1%

The consensus sees slower growth at 5.6 percent on year in

Q1 versus 6.9 percent in Q4.

China Merchandise Trade for March (ANYTIME)

Consensus Forecast, Balance: $108.0 B

Consensus Range, Balance: $105 B to $119.1 B

Consensus Forecast, Imports - Y/Y: 14.9%

Consensus Range, Imports - Y/Y: 10.1% to 14.9%

Consensus Forecast, Exports - Y/Y: 10.3%

Consensus Range, Exports - Y/Y: 3.5% to 15.5%

The surplus is expected at $108 billion for March.

Sweden CPI for March (Tue 0800 CEST; Tue 0600 GMT; Tue

0200 EDT)

Consensus Forecast, M/M: -0.6%

Consensus Forecast, Y/Y: 0.6%

The consensus sees CPI up 0.6 percent on year in March, up

from 0.5 percent in February.

US NFIB Small Business Optimism Index for March (Tue

0600 EDT; Tue 1000 GMT)

Consensus Forecast, Index: 97.5

Consensus Range, Index: 96.3 to 98.5

The consensus looks for the index to fall back to 97.5 in

March from 98.8 in February as rising energy prices hit sentiment.

US PPI-Final Demand for March (Tue 0830 EDT; Tue 1230

GMT)

Consensus Forecast, PPI-FD - M/M: 1.2%

Consensus Range, PPI-FD - M/M: 1.0% to 2.3%

Consensus Forecast, PPI - Y/Y: 4.7%

Consensus Range, PPI - Y/Y: 4.1% to 5.9%

Consensus Forecast, Ex-Food & Energy - M/M: 0.5%

Consensus Range, Ex-Food & Energy - M/M: 0.3% to 0.7%

Consensus Forecast, Ex-Food & Energy - Y/Y: 4.2%

Consensus Range, Ex-Food & Energy - Y/Y: 3.7% to 4.3%

A hideous 1.2 percent one-month rise in PPI-FD is the

expectation based on surging energy costs. Ex-food & energy, the consensus

sees 0.5 percent on the month, not a pretty picture. On year, the consensus

sees total PPI-FD up 4.7 percent and up 4.2 percent ex-food & energy.

Wednesday

Japan Machinery Orders for February (Wed 0850 JST;

Tue 2350 GMT; Tue 1950 EDT)

Consensus Forecast, M/M: -0.1%

Consensus Range, M/M: -2.0% to 3.9%

Consensus Forecast, Y/Y: 12.0%

Consensus Range, Y/Y: 7.5% to 14.0%

Japan's core machinery orders, a key leading indicator of

business investment in equipment and software, are expected to edge down 0.1

percent in February, marking a second straight monthly decline after a 5.5

percent drop in January.

Still, the underlying trend in machinery orders is seen as

firm, supported by demand for machine tools. The impact of heightened Middle

East tensions following U.S. and Israeli attacks on Iran in late February is

viewed as having had only a limited effect on orders. Orders are also likely to

be underpinned by steady services-sector demand for computers, driven by

ongoing automation and digitalization efforts to ease labor shortages.

On a year-on-year basis, machinery orders are expected to

rise for a third straight month in February, increasing 12.0 percent after a

13.7 percent gain in January.

India WPI for March (Wed 0830 CEST; Wed 0630GMT; Wed

0230 EDT

Consensus Forecast, Y/Y: 3.40%

Consensus Range, Y/Y: 3.04% to 3.5%

The consensus sees wholesale prices up 3.40 percent on year

in March versus 2.13 percent in February.

France CPI for March (Wed 0845 CEST; Wed 0645 GMT; Wed

0245 EDT)

Consensus Forecast, M/M: 0.9%

Consensus Range, M/M: 0.9% to 0.9%

Consensus Forecast, Y/Y: 1.7%

Consensus Range, Y/Y: 1.7% to 1.7%

The consensus looks for no revision from the flash at 0.9

percent on month and 1.7 percent on year for March.

Eurozone Industrial Production for February (Wed 1100

CEST; Wed 0900 GMT; Wed 0500 EDT)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: -0.2% to 0.8%

Consensus Forecast, Y/Y: -1.0%

Consensus Range, Y/Y: -1.6% to -1.4%

Output expected to rebound by 0.4 percent in February after

falling 1.5 percent on month in January. Output still seen down 1.0 percent on

year after falling by 1.2 percent in January.

India CPI for March (Wed 1600 IST; Wed 1030 GMT; Wed

0630 EDT)

Consensus Forecast, Y/Y: 3.43%

Consensus Range, Y/Y: 3.40% to 3.48%

CPI seen up 3.43 percent on year in March after 3.21 percent

in February.

Canada Manufacturing Sales for February (Wed 0830

EDT; Wed 1230 GMT)

Consensus Forecast, M/M: 3.8%

Consensus Range, M/M: 3.5% to 3.8%

Forecasters agree with the Stats Canada preliminary estimate

calling for sales to rebound by 3.8 percent on the month in February after

dropping 3.0 percent in January.

US Empire State Manufacturing Index for April (Wed 0830

EDT; Wed 1230 GMT)

Consensus Forecast, Index: -2.0

Consensus Range, Index: -3.1 to 3.3

Manufacturing seen sluggish with the index barely in

contraction territory at minus 2.0 for April, down from an already unimpressive

minus 0.2 in March.

US Imports and Export Prices for March (Wed 0830 EDT;

Wed 1230 GMT)

Consensus Forecast, Import Prices - M/M: 2.1%

Consensus Range, Import Prices - M/M: 0.4% to 2.9%

Consensus Forecast, Export Prices - M/M: 1.7%

Consensus Range, Export Prices - M/M: 1.0% to 3.2%

The consensus sees rising fuel costs lifting import prices

by 2.1 percent and export prices by 1.7 percent on the month!

US Housing Market Index for April (Wed 1000 EDT; Wed 1400

GMT)

Consensus Forecast, Index: 37

Consensus Range, Index: 36 to 38

Homebuilder sentiment remains depressed with the index seen

at 37 in April, down from 38 in March.

Thursday

Australia Labour Force Survey for March (Thu 1130 AEST;

Thu 0130 GMT; Wed 2130 EDT)

Consensus Forecast, Employment - M/M: 17.8K

Consensus Range, Employment - M/M: 5K to 35K

Consensus Forecast, Unemployment Rate: 4.3%

Consensus Range, Unemployment Rate: 4.1% to 4.4%

Forecasters see a moderate 17,800 increase in employment for

the first part of March with the ill effects of the energy price shock yet to

appear. No change expected in the jobless rate at 4.3 percent.

China Fixed Asset Investment for March (Thu 1000 CST;

Thu 0200 GMT; Wed 2200 EDT)

Consensus Forecast, Year to Date on Y/Y Basis: 1.9%

Consensus Range, Year to Date on Y/Y Basis: 1.8% to 2.0%

Stable growth expected with FAI up 1.9 percent versus 1.8

percent in February.

China GDP for First Quarter (Thu 1000 CST; Thu 0200

GMT; Wed 2200 EDT)

Consensus Forecast, Q/Q: 1.4%

Consensus Range, Q/Q: 0.8% to 1.4%

Consensus Forecast, Y/Y: 4.8%

Consensus Range, Y/Y: 4.6% to 5.0%

Moderate growth is the call with GDP up 4.8 percent on year

in Q1 versus 4.5 percent in Q4.

China Industrial Production for March (Thu 1000 CST; Thu

0200 GMT; Wed 2200 EDT)

Consensus Forecast, Y/Y: 5.4%

Consensus Range, Y/Y: 4.8% to 6.3%

The consensus sees output up 5.4 percent on year in March.

China Retail Sales for March (Thu 1000 CST; Thu 0200

GMT; Wed 2200 EDT)

Consensus Forecast, Y/Y: 2.4%

Consensus Range, Y/Y: 2.1% to 3.5%

Annual sales growth seen at 2.4 percent in March versus 2.8

percent in February.

UK Monthly GDP for February (Thu 0700 GMT; Thu 0200 EDT)

Consensus Forecast, M/M: 0.15%

Consensus Range, M/M: 0.1% to 0.2%

The consensus looks for very modest growth at 0.15 percent

on the month.

Italy CPI for March (Thu 1000 CEST; Thu 0800

GMT; Thu 0400 EDT)

Consensus Forecast, M/M: 0.5%

Consensus Range, M/M: 0.5% to 0.5%

Consensus Forecast, Y/Y: 1.7%

Consensus Range, Y/Y: 1.7% to 1.7%

No revision expected from the flash for the final at 0.5

percent on month and 1.7 percent on year in March.

Eurozone HICP for March (Thu 1100 CEST; Thu 0900 GMT;

Thu 0500 EDT)

Consensus Forecast, HICP - M/M: 1.2%

Consensus Range, HICP - M/M: 1.2% to 1.2%

Consensus Forecast, HICP - Y/Y: 2.5%

Consensus Range, HICP - Y/Y: 2.5% to 2.5%

Consensus Forecast, Narrow Core - Y/Y: 2.3%

Consensus Range, Narrow Core - Y/Y: 2.3% to 2.3%

No revision expected from the flash at 1.2 percent on month

and 2.5 percent on year.

US Jobless Claims for Week 04/11 (Thu 0830 EDT; Thu

1230 GMT)

Consensus Forecast, Initial Claims - Level: 215K

Consensus Range, Initial Claims - Level: 209K to 230K

Claims seen back down at 215K after jumping by 16k to 219K

in previous week.

US Philadelphia Fed Manufacturing Index for April (Thu

0830 EDT; Thu 1230 GMT)

Consensus Forecast, Index: 12.0

Consensus Range, Index: 7.0 to 20.3

Index seen down in April but still solidly in expansion at

12.0 versus 18.1 in March.

US Industrial Production for March (Thu 0915 EDT; Thu

1315 GMT)

Consensus Forecast, Industrial Production - M/M: 0.1%

Consensus Range, Industrial Production - M/M: -0.3%

to 0.5%

Consensus Forecast, Manufacturing Output - M/M: 0.3%

Consensus Range, Manufacturing Output - M/M: -0.5% to

0.5%

Consensus Forecast, Capacity Utilization Rate: 76.3%

Consensus Range, Capacity Utilization Rate: 76.1% to

76.7%

Modest increase in industrial output expected at 0.1 percent

with manufacturing up 0.3 percent and capacity utilization flat at 76.3 percent

for March.

Friday

Canada Housing Starts for March (Fri 0815 EDT; Fri 1215

GMT)

Consensus Forecast, Annual Rate: 240K

Consensus Range, Annual Rate: 230K to 250K

Starts expected softer at 240K in March versus 251K in

February.

|