|

The Week Ahead: Highlights

Asia-Pacific Preview

Australia Inflation, China Purchasers Reports Ahead

By Brian Jackson, Econoday Economist

Monthly CPI data for Australia will be a key focus for the

Asia-Pacific region. Although next week's data will likely be impacted by the

spike in fuel prices in response to the Iran conflict, officials at the Reserve

Bank of Australia will also be looking for evidence of broader price pressures.

Headline inflation has now been above the RBA's target range of two percent to

three percent for seven consecutive months, suggesting further policy

tightening will likely be considered in upcoming meetings. Quarterly producer

price inflation data will also be published next week.

Official PMI survey data for China will provide an early indication of

conditions in April. With the survey showing activity was already subdued in

March, the impact of the Iran conflict could weaken conditions further. South

Korea industrial production, Hong Kong trade and Taiwan GDP data will also be

published next week.

Europe Preview

Watching Impact of Energy Price Shock on Inflation

By Marco Babic, Econoday Economist

The week ahead sees a spate of inflation data for Europe

which will be closely watched given the situation In the Middle East. For some

time, consumer prices have been relatively subdued largely helped by falling

energy prices, which has kept consumer inflation well within the comfort zone

of the European Central Bank. Since the outbreak of hostilities at the end of

February, that scenario is no longer holding.

In Germany, Europe's largest economy, inflation was running at 2.7 percent

year-on-year in March, with the Harmonized Index at 2.8 percent. In France, it

was more subdued at 1.7 percent year-on-year, although the harmonized rate was

at 2.0 percent, just at the upper level of what the ECB will find

uncomfortable.

On Thursday, the April results for Europe will be released by Eurostat. In

March inflation ran at 2.6 percent while the narrow core was at 2.3 percent.

There are few, if any, reasons to think that inflation will have moderated in

April given the ongoing tensions surrounding the bottlenecks in the Strait of

Hormuz.

PMI results for April have shown anecdotal evidence that prices are becoming a

big consideration for companies. One upshot of that has been an increase in

production and order books as firms race to secure necessary inputs for their

production lines. This shows that companies are expecting a prolonged bout of

higher prices, and the question like that with tariffs is when and by how much

suppliers can pass along higher costs to their customers.

While core readings will show the degree of energy prices' impact on inflation,

the fact is that consumers won't care what the core rate is as they feel the

stress of higher energy prices. That will most likely impact discretionary

consumer spending and have a negative impact on GDP in the second quarter.

The question is when and how the ECB, the Swiss National Bank, and other

European Central banks respond to higher prices as they now have the headache

of trying to deal not just with inflation but also economic slowdown and stave

off stagflation.

US Preview

Federal Reserve Policy-makers Weigh Fallout from Iran War

By Theresa Sheehan, Econoday Economist

The FOMC meetings on Tuesday and Wednesday (April 28-29) are

coming against a backdrop of lengthening geopolitical uncertainty related to

the war on Iran. It is increasingly difficult to argue that the surge in oil

prices would reverse in the near term, and that impacts on the domestic and

global economies would be short-lived. Rosy predictions of positive outcomes

are looking unrealistic and only adding to the noise of trying to make sense of

events. Absent a catastrophic exogenous event, the FOMC will leave rates

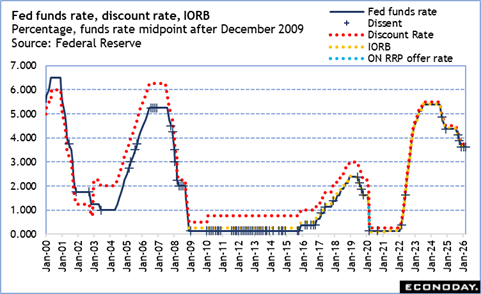

unchanged for a fourth meeting in a row at 3.50-3.75 percent.

The FOMC will be trying to set policy in accordance with the

dual mandate for maximum employment and price stability. It will have to weigh

the risks in balancing the two. Concerns are growing that the moderate

underlying pace of expansion is flagging and the consequences for the labor

market. The "low hire, no fire" situation may be slipping into "no hire, no

fire". While this is not the most desirable condition for the employment

mandate, it is numbers related to inflation that will be the larger determinant

of meeting decision.

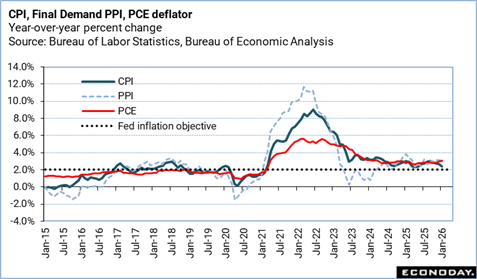

The March reports for the CPI and final-demand PPI did not

capture the full impact of the sudden and large increase in energy prices and

the first wave to pass-through to consumers and producers. The April indexes

for inflation will not be available until weeks after the meeting. However, the

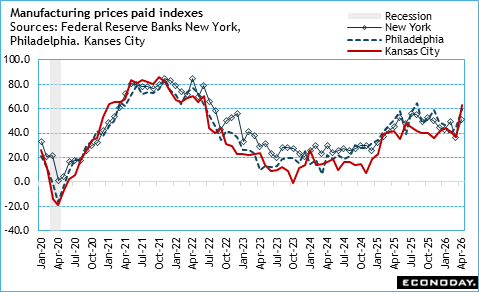

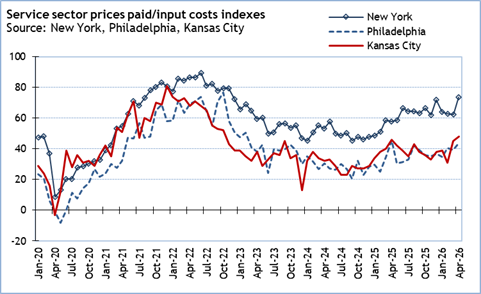

April surveys of the manufacturing and service sectors point to big jumps input

costs that won't be expected to come down any time soon and will force

cost-cutting and/or price increases. Businesses could do either or both.

Households will face lower discretionary income and or weaker job security. The

FOMC will have to assess the risks to inflation as elevated, and probably not

just the "somewhat" that has been in use since July 24, 2024.

The FOMC is scheduled to release the meeting statement at

14:00 ET on Wednesday. The statement will be carefully parsed to see if a

majority of the FOMC are turning more hawkish on inflation. Stephen Miran

remains a holdover on the Fed board after the expiration of his term on January

31, 2026. It seems he plans to remain there until a new chair is confirmed. It

would be no surprise if he registered his sixth straight dissent in the FOMC

vote in favor of lowering the fed funds target rate.

In the meantime, Kevin Warsh had his confirmation hearing

for government and Fed chair on April 21. Even with the Department of Justice

saying it has suspended its criminal investigation of the Fed, it appears

likely his confirmation will be caught in committee for a while yet and without

a vote in the full Senate. It looks increasingly like Jerome Powell will be chair

pro tem after the expiration of his term as chair in mid-May. The logjam in the

Senate could be cleared by the June 16-17 FOMC meeting. It is not absolutely

certain that the April 29 press briefing at 14:30 ET will be Powell's last as chair.

The central theme for monetary policy of the upcoming press

briefing will center around uncertainty and the inflation outlook, and the

possibility of moving toward a recession. Powell will also be asked questions

regarding his plans. He will likely reiterate his intention to remain as a

governor until the matter around the accusations of mismanagement of the Fed

building renovations are fully resolved. He will avoid adding to any

controversy about Fed staffing and/or relations with Congress and the President.

The Week Ahead: Econoday Consensus Forecasts

Monday

Germany Gfk Consumer Climate Index for May (Mon 0600

GMT; Mon 0200 EDT)

Consensus Forecast, Index: -29.3

Consensus Range, Index: -31.0 to -29.0

The consensus sees a gloomier consumer facing rising energy

costs with the index down to minus 29.3 in May from minus 28.0 in April.

Tuesday

Japan Unemployment Rate for March (Tue 0830 JST; Mon 2330

GMT; Mon 1930 EDT)

Consensus Forecast, Rate: 2.6%

Consensus Range, Rate: 2.6% to 2.7%

Japan's seasonally adjusted unemployment rate is expected to

be unchanged at 2.6 percent in March from February. After rising to 2.7 percent

in January, the rate has held steady at 2.6 percent for five months from August

to December, highlighting firm labor market conditions amid persistent labor

shortages.

In February, employment rose 110,000 from a year earlier to

67.79 million, marking the first increase in two months. The number of

unemployed climbed by 150,000 to 1.80 million, extending gains to a seventh

straight month.

Japan Bank of Japan Announcement (Tue 1130 JST; Tue

0230 GMT; Mon 2230 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 0.75%

Consensus Range, Level: 0.75% to 0.75%

The Bank of Japan's nine-member board is expected to leave

the target for the overnight interest at 0.75 percent in a majority or

unanimous vote, pointing to the uncertainty generated by the Mideast conflict.

It would follow "no change" decisions in an 8 to 1 vote in March and January.

The bank conducted its first rate hike in six meetings in December by raising it

by 25 basis points (0.25 percentage point) to a 30-year high in a unanimous

vote.

The board is likely to repeat that it will continue raising rates if growth and

inflation evolve in line with its medium-term outlook, noting that real

interest rates are at "significantly low levels." The BOJ has been lifting the

policy rate only gradually toward a more neutral level of at least 1 percent,

noting that many firms are likely to continue raising wages into fiscal 2026

that began on April 1.

India Industrial Production for March (Tue 1600 IST; Tue

1030 GMT; Tue 0630 EDT)

Consensus Forecast, Y/Y: 3.0%

Consensus Range, Y/Y: 2.7% to 3.0%

Much slower growth seen at 3.0 percent in March versus 5.2

percent in February.

US Consumer Confidence for April (Tue 1000 EDT; Tue

1400 GMT)

Consensus Forecast, Index: 89.4

Consensus Range, Index: 87.0 to 90.4

Confidence expected to take a hit from worries about rising

prices and uncertainty flowing from the Iran war. The consensus sees the index

down at 89.4 in April from 91.8 in March.

Wednesday

Australia Monthly CPI for March (Wed 1130 AEST; Wed 0130

GMT; Tue 2130 EDT)

Consensus Forecast, Y/Y: 4.8%

Consensus Range, Y/Y: 4.4% to 4.8%

Energy price shock showing up in CPI with the annual rate

expected up to 4.8 percent in March from 3.7 percent in February.

Eurozone M3 Money Supply for March (Wed 1000 CEST; Wed

0800 GMT; Wed 0400 EDT)

Consensus Forecast, Y/Y-3-Month Moving Average: 3.1%

Consensus Range, Y/Y-3-Month Moving Average: 3.0% to 3.1%

Not much change seen in money growth, expected at 3.1

percent versus 3.0 percent a month earlier.

Eurozone EC Economic Sentiment for April (Wed 1100 CEST;

Wed 0900 GMT; Wed 0500 EDT)

Consensus Forecast, Economic Sentiment: 95.6

Consensus Range, Economic Sentiment: 94.1 to 96.3

Consensus Forecast, Industry Sentiment: -7.0

Consensus Range, Industry Sentiment: -9.0 to -6.9

Sentiment expected to show a decline to 95.6 in April from

96.6 in March amid concern over rising energy costs.

Germany CPI for April (Wed 1400 CEST; Wed 1200 GMT; Wed

0800 EDT)

Consensus Forecast, M/M: 0.7%

Consensus Range, M/M: 0.6% to 1.0%

Consensus Forecast, Y/Y: 2.9%

Consensus Range, Y/Y: 2.7% to 3.3%

Consensus Forecast, HICP - M/M: 0.9%

Consensus Range, HICP - M/M: 0.7% to 1.1%

Consensus Forecast, HICP - Y/Y: 3.1%

Consensus Range, HICP - Y/Y: 3.0% to 3.4%

The month on month increase in CPI seen up again by 0.7

percent, something of a relief after a 1.1 percent surge on the month in March,

but still a remarkable increase amid rising energy prices.

US Durable Goods Orders for March (Wed 0830 EDT; Wed

1230 GMT)

Consensus Forecast, New Orders - M/M: 0.5%

Consensus Range, New Orders - M/M: 0.3% to 1.2%

Consensus Forecast, Ex-Transportation - M/M: 0.4%

Consensus Range, Ex-Transportation - M/M: 0.3% to

1.8%

A moderate increase seen with orders expected up 0.5 percent

and 0.4 percent, ex-transportation, in March from February.

US Housing Starts and Permits for February (Wed 0830

EDT; Wed 1230 GMT)

Consensus Forecast, Starts - Annual Rate: 1.37 M

Consensus Range, Starts - Annual Rate: 1.341 M to 1.40

M

Consensus Forecast, Permits - Annual Rate: 1.39 M

Consensus Range, Permits - Annual Rate: 1.39 M to 1.39

M

US Housing Starts and Permits for March (Wed 0830

EDT; Wed 1230 GMT)

Consensus Forecast, Starts - Annual Rate: 1.40 M

Consensus Range, Starts - Annual Rate: 1.324 M to 1.438

M

Consensus Forecast, Permits - Annual Rate: 1.398 M

Consensus Range, Permits - Annual Rate: 1.35 M to 1.40

M

Rising cost pressures expected to depress housing starts to

an annual 1.37 million in February and 1.40 million rate in March from 1.487 million

in January.

US International Trade in Goods (Advance) for March (Wed

0830 EDT; Wed 1230 GMT)

Consensus Forecast, Balance: -$87.8 B

Consensus Range, Balance: -$89.5 B to -$80.2 B

Goods trade gap seen up at $87.8 billion in March versus

$84.6 billion in February.

Canada Bank of Canada Announcement (Wed 0945 EDT; Wed

1445 GMT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 2.25%

Consensus Range, Level: 2.25% to 2.25%

BOC on hold with growth holding up surprisingly well and

policy-makers looking past the spike in gas prices.

US FOMC Announcement (Wed 1400 EDT; Wed 1800 GMT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Federal Funds Rate - Target Range: 3.5%

- 3.75%

Consensus Range, Federal Funds Rate - Target Range: 3.5%

- 3.75% to 3.5% -3.75%

Fed seen still in wait and see mode and no doubt pleased

that the job market appears to have stabilized. Still watching for progress on

inflation after the tariff episode, now interrupted by an energy price shock.

Thursday

Japan Industrial Production for March (Wed 0850 JST;

Tue 2350 GMT; Tue 1950 EDT)

Consensus Forecast, M/M: 0.7%

Consensus Range, M/M: -1.0% to 2.5%

Consensus Forecast, Y/Y: 3.0%

Consensus Range, Y/Y: 0.0% to 5.3%

Japan's industrial output is expected to rebound in March,

marking the first monthly increase in two months as the impact of Middle East

geopolitical tensions appears limited and exports picked up during the month.

Industrial production is seen rising 0.7 percent on the

month in March after a revised 2.0 percent drop in February, compared with an

initial 2.1% decline. The February contraction was initially driven by declines

in trucks, engines, aluminum products and liquid crystal display panels. The

subsequent upward revision reflected increases in pharmaceuticals and auto

parts, while output in the food and tobacco industries fell.

On a year-on-year basis, output is expected to rise for a

fourth consecutive month in March, increasing 3.0 percent after a revised 0.4

percent gain in February (initially 0.3 percent).

Japan Retail Sales for March (Wed 0850 JST; Tue 2350

GMT; Tue 1950 EDT)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: -0.8% to 1.4%

Consensus Forecast, Y/Y: 1.0%

Consensus Range, Y/Y: -0.4% to 1.8%

Japan's retail sales are seen rising for the first time in

two months in March after falling in the previous month, weighed down by

sluggish clothing sales and a sharp drop in fuel prices following the

government's removal of decades-old surcharges at the end of 2025.

Retail sales are expected to increase 1.0 percent on the

year in March after a revised 0.1 percent decline in February (initially -0.2

percent). Sales are projected to rebound amid stronger department store sales.

Auto sales also appear to have picked up, with the decline in new passenger car

registrations narrowing from the previous month, while the drop in fuel

retailing is seen moderating.

On a month-on-month basis, sales are expected to rise 0.4

percent in March after falling 2.0 percent in the previous month.

China CFLP Composite PMI for March (Wed 0930 CST; Wed

0130 GMT; Tue 2130 EDT)

Consensus Forecast, Manufacturing Index: 50.1

Consensus Range, Manufacturing Index: 50.1 to

50.4

Consensus Forecast, Non-Manufacturing Index: 49.9

Consensus Range, Non-Manufacturing Index: 49.8 to 49.9

Business activity expected flat to lower with the

manufacturing index at 50.1 in March versus 50.4 in February and services down

to marginal contraction at 49.9 from 50.1.

France GDP Flash for First Quarter (Thu 0730 CEST;

Thu 0530 GMT; Thu 0130 EDT)

Consensus Forecast, Q/Q: 0.2%

Consensus Range, Q/Q: 0.1% to 0.2%

Growth expected to continue at modest 0.2 percent rate in

Q1.

Germany Retail Sales for March (Thu 0800 CEST; Thu 0600

GMT; Thu 0200 EDT)

Consensus Forecast, M/M: -0.4%

Consensus Range, M/M: -0.8% to 0.3%

Another month of losses expected with sales down 0.4 percent

in March after minus 0.6 percent in February.

Germany Unemployment Rate for April (Thu 0955 CEST;

Thu 0755 GMT; Thu 0355 EDT)

Consensus Forecast, Rate: 6.3%

Consensus Range, Rate: 6.3% to 6.4%

More of the same expected with the jobless rate flat at 6.3

percent in April.

Germany GDP Flash for First Quarter (Thu 1000 CEST;

Thu 0900 GMT; Thu 0400 EDT)

Consensus Forecast, Q/Q: 0.1%

Consensus Range, Q/Q: -0.2% to 0.2%

Consensus Forecast, Y/Y: 0.2%

Consensus Range, Y/Y: 0.2% to 0.6%

The consensus sees a sluggish 0.1 percent rise on quarter in

Q1 and a marginal 0.2 percent increase on year.

Eurozone GDP Flash for First Quarter (Thu 1100 CEST;

Thu 0900 GMT; Thu 0500 EDT)

Consensus Forecast, Q/Q: 0.2%

Consensus Range, Q/Q: 0.1% to 0.2%

Consensus Forecast, Y/Y: 0.9%

Consensus Range, Y/Y: 0.8% to 1.1%

GDP expected at 0.2 percent in Q1 versus 0.3 percent in Q4.

Eurozone HICP Flash for April (Thu 1100 CEST; Thu 0900

GMT; Thu 0500 EDT)

Consensus Forecast, HICP - Y/Y: 3.1%

Consensus Range, HICP - Y/Y: 2.6% to 3.5%

Consensus Forecast, Narrow Core - Y/Y: 2.3%

Consensus Range, Narrow Core - Y/Y: 2.2% to 2.4%

HICP seen up 3.1 percent on year in April versus 2.6 percent

in March, showing energy price shock. Narrow core seen unchanged at 2.3

percent, thankfully.

Eurozone Unemployment Rate for March (Thu 1100 CEST;

Thu 0900 GMT; Thu 0500 EDT)

Consensus Forecast, Rate: 6.2%

Consensus Range, Rate: 6.2% to 6.2%

No change seen at 6.2 percent in the jobless rate.

UK BoE Announcement & Minutes (Thu 1200 BST; Thu 0700

EDT)

Consensus Forecast, Bank Rate - Change: 0 bp

Consensus Range, Bank Rate - Change: 0 bp to 0 bp

Consensus Forecast, Bank Rate - Level: 3.75%

Consensus Range, Bank Rate - Level: 3.75% to 3.75%

BOE officials making it clear they want to keep rates where

they are for now.

Eurozone ECB Announcement (Thu 1415 CEST; Thu 1215

GMT; Thu 0815 EDT)

Consensus Forecast, Refi Rate Change: 0 bp

Consensus Range, Refi Rate Change: 0 bp to 0 bp

Consensus Forecast, Refi Rate Level: 2.15%

Consensus Range, Refi Rate Level: 2.15% to 2.15%

Consensus Forecast, Deposit Rate Change: 0 bp

Consensus Range, Deposit Rate Change: 0 bp to 0 bp

Consensus Forecast, Deposit Rate Level: 2.00%

Consensus Range, Deposit Rate Level: 2.00% to 2.00%

Until it becomes clear how long the energy shock will last,

or something else changes the picture, forecasters see the ECB and the rest of

the major central banks on hold.

Canada Monthly GDP for February (Thu 0830 EDT; Thu

1230 GMT)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: 0.2% to 0.3%

Forecasters agree, as usual, with the Stats Canada

preliminary estimate calling for a gain of 0.2 percent on the month in

February.

US GDP for First Quarter (Thu 0830 EDT; Thu 1230 GMT)

Consensus Forecast, Quarter over Quarter - Annual Rate:

2.1%

Consensus Range, Quarter over Quarter - Annual Rate: 1.0%

to 2.8%

Consensus Forecast, Personal Consumption Expenditures -

Annual Rate: 1.5%

Consensus Range, Personal Consumption Expenditures -

Annual Rate: 1.0% to 1.6%

The consensus sees a return to healthy growth at 2.1 percent

after a cutback in government spending hit growth in Q4.

US Jobless Claims for Week 04/25 (Thu 0830 EDT; Thu

1230 GMT)

Consensus Forecast, Initial Claims - Level: 212K

Consensus Range, Initial Claims - Level: 205K to 220K

The consensus sees claims down to 212K in the week, closer

to the 4-week moving average of 210,75K, from 214 last week.

US Personal Income and Outlays for March (Thu 0830

EDT; Thu 1230 GMT)

Consensus Forecast, Personal Income - M/M: 0.3%

Consensus Range, Personal Income - M/M: 0.2% to 0.8%

Consensus Forecast, Personal Consumption Expenditures -

M/M: 0.9%

Consensus Range, Personal Consumption Expenditures - M/M:

0.3% to 1.0%

Consensus Forecast, PCE Price Index - M/M: 0.7%

Consensus Range, PCE Price Index - M/M: 0.7% to 0.8%

Consensus Forecast, PCE Price Index - Y/Y: 3.5%

Consensus Range, PCE Price Index - Y/Y: 3.5% to 3.5%

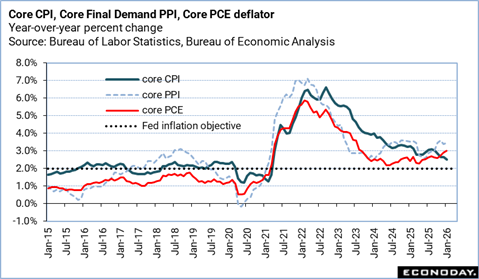

Consensus Forecast, Core PCE Price Index - M/M: 0.3%

Consensus Range, Core PCE Price Index - M/M: 0.3% to

0.7%

Consensus Forecast, Core PCE Price Index - Y/Y: 3.2%

Consensus Range, Core PCE Price Index - Y/Y: 2.9% to

3.5%

A nasty inflation reading with PCE prices expected up 0.7

percent on the month and 3.5 percent on year. Core seen up 0.3 percent on the

month and 3.2 percent on year, not reassuring at all.

US Employment Cost Index for First Quarter (Thu 0830

EDT; Thu 1230 GMT)

Consensus Forecast, Q/Q: 0.8%

Consensus Range, Q/Q: 0.7% to 0.9%

Relatively modest 0.8 percent increase seen on the quarter,

suggesting inflation pressures evident elsewhere remain restrained in the

employment market where workers aren't feeling so confident about demanding

more pay.

US Chicago PMI for April (Thu 0830 EDT; Thu 1230 GMT)

Consensus Forecast, Index: 53.3

Consensus Range, Index: 51.0 to 55.7

Forecasters see the Chicago PMI showing odd strength with

the index up to 53.3 in April from 52.8 in March.

Friday

Japan Tokyo CPI for April (Fri 0830 JST; Thu 2330

GMT; Thu 1930 EDT)

Consensus Forecast, CPI - Y/Y: 1.6%

Consensus Range, CPI - Y/Y: 1.4% to 1.9%

Consensus Forecast, Ex-Fresh Food - Y/Y: 1.8%

Consensus Range, Ex-Fresh Food - Y/Y: 1.6% to 2.0%

Consensus Forecast, Ex-Fresh Food & Energy - Y/Y:

2.3%

Consensus Range, Ex-Fresh Food & Energy - Y/Y: 2.0%

to 2.5%

The Tokyo consumer price index, a leading indicator of

nationwide price trends, is expected to edge higher across the two main

measures in April. The closely watched core CPI is seen accelerating for the

first time in six months but is likely to remain below the Bank of Japan's 2

percent inflation target for a third straight month.

The core CPI, which excludes fresh food, is projected to

rise 1.8 percent in April from a near two-year low of 1.7 percent a month

earlier. The underlying weakness of the yen continues to pose upside inflation

risks.

Elsewhere, the overall CPI is expected to pick up for the

first time since October last year, rising 1.6 percent on the year in April

after increasing 1.4 percent in March. The core-core index, which excludes

fresh food and energy, is seen holding steady at 2.3 percent.

US ISM Manufacturing Index for April (Fri 1000 EDT;

Fri 1400 GMT)

Consensus Forecast, Index: 53.0

Consensus Range, Index: 51.9 to 56.0

Another month of moderate growth is the call for ISM

manufacturing with the index expected u at 53.0 in April from 52.7 in March.

|