|

The Week Ahead: Highlights

US Preview

Beige Book, Payrolls Report Key

By Theresa Sheehan, Econoday Economist

There are two reports that will dominate perceptions of

conditions in the US economy in the June 1 week.

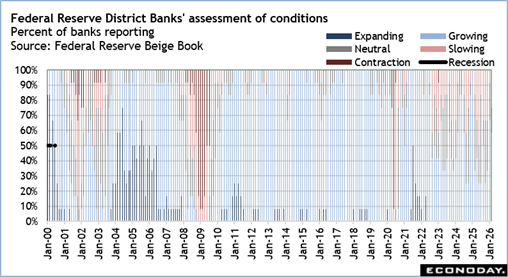

First, the Fed's beige book at 14:00 ET on Wednesday will

provide a snapshot of conditions across the Fed's 12 district banks. The

upcoming release will cover the period between early April and mid-May. The

anecdotal evidence about the economy is likely to reflect high levels of

uncertainty regarding the direction of prices and how long and where the

effects of sharp increases oil prices will be a factor. The report will

highlight shifts in consumer spending away from discretionary spending and

places where rising interest rates are having an impact like the housing market

and purchases of big-ticket items like home appliances and electronics. It will

also offer a qualitative assessment of the labor market that will inform

policymakers' views at the next FOMC meeting on June 17-18. Overall, the report

should show the US economy is treading water until some clarity emerges for the

geopolitical outlook.

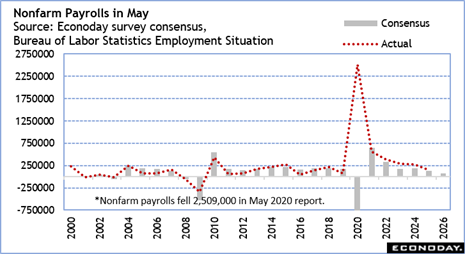

Second, the May employment report at 8:30 ET on Friday may

not be typical for May. The month is one when leisure and hospitality starts

adding jobs ahead of the summer vacation period and companies hire college

graduates. Less of this is expected as businesses are cautious about the

direction of consumer spending on travel the word staycation is probably

going to be more popular with gas prices at current levels. Other businesses

will be assessing their staffing needs carefully and looking to fill only essential

spots. The adoption of AI tools may also be a factor in restraining payroll

growth. It remains to be seen if the hunger for skilled workers in the

healthcare sector is satisfied. Nonetheless, with relatively little layoff

activity, unemployment rates are not going higher. A variation of a tenth from

month-to-month is not immediately significant.

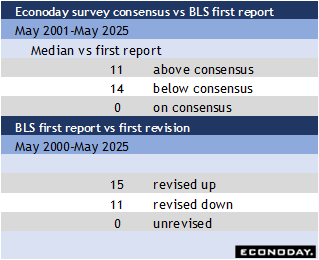

Forecasts for May have a slight tendency to come in below

consensus but are also likely to be revised up in the coming months. The survey

reference period closed on May 16. With the Memorial Day observance relatively

early on May 26, hiring of seasonal workers should be captured.

Asia-Pacific Preview

Busy Data Week plus Reserve Bank of India Policy Decision

Ahead

By Brian Jackson, Econoday Economist

May PMI surveys will be the main focus in the Asia-Pacific

region, with the Iran conflict still weighing on activity and sentiment. China

will release its official PMI ahead of the main private-sector survey and both

will be watched after they have shown some divergence in recent months.

Accompanying the publication of key activity data earlier this month, officials

revised their policy guidance, pledging to "implement a more proactive

fiscal policy and an appropriately accommodative monetary policy". Weakness in

these PMI surveys may strengthen the case for some policy easing in the weeks

ahead.

Elsewhere in the region, the impact of the Iran conflict has been offset and

even outweighed by ongoing strong demand for semiconductor and AI technology.

South Korea and Taiwan, in particular, are benefiting from this demand, with

their PMI surveys last month also showing firms had increased production to

safeguard against potential supply disruptions and cost increases. India and

Singapore PMIs also showed strong conditions last mont, though Hong Kong's PMI

indicated contraction in its aggregate economy for the second consecutive

month.

Another key focus will be the Reserve Bank of India policy decision. The RBI's

last policy meeting was in early April, but the Iran-driven surge in fuel

prices since then has pushed wholesale price inflation up from 3.9 percent in

March to 8.3 percent in April, its highest level since 2022. Having left

rates on hold in its last two meetings, the consensus is for no change again

next week, but officials may provide some guidance on the extent to which they

consider this increase in wholesale prices will impact the outlook for consumer

inflation.

Australia will publish GDP data for the three months March next week, with

other data showing strong investment growth over the quarter but the first

monthly trade deficit since 2017 in the last month of the quarter. Australia

will also report April trade data next week, while India will also release its

GDP report. Taiwan inflation data will be published ahead of the quarterly

policy meeting later in the month.

The Week Ahead: Econoday Consensus Forecasts

Sunday

China CFLP PMI Manufacturing/Services for May

Consensus Forecast, Manufacturing Index: 50.0

Consensus Range, Index: 50.0 to 50.2

Consensus Forecast, Services Index: 49.5

Consensus Range, Index: 49.5 to 49.5

Manufacturing is expected down slightly to 50.0 in May

versus 50.3 in April. Services is seen pretty flat in marginal contraction at 49.5

in May versus 49.4 in April.

Monday

China PMI Manufacturing for May (Mon 0945 CST; Mon

0145 GMT; Sun 2145 EDT)

Consensus Forecast, Index: 51.3

Consensus Range, Index: 50.4 to 51.6

Manufacturing business likely to show slower growth at 51.3 in

the May, down from 52.2 in April.

Germany Retail Sales for April (Mon 0800 CEST; Mon 0600

GMT; Mon 0200 EDT)

Consensus Forecast, M/M: 0.3%

Consensus Range, M/M: -0.5% to 1.1%

Consensus Forecast, Y/Y: -1.4%

Consensus Range, Y/Y: -1.4% to -1.4%

The consensus sees sales up 0.3 percent on the month in

April after falling 2.0 percent in March. Sales on year are seen down 1.4

percent after dropping 2.0 percent in March on year.

France PMI Manufacturing Final for May (Mon 0850

CEST; Mon 0650 GMT; Mon 0250 EDT)

Consensus Forecast, Index: 48.9

Consensus Range, Index: 48.9 to 48.9

Manufacturing business expected to show contraction at 48.9

in the May final reading, unrevised from 48.9 in the flash and down from 52.8

in the April final.

Switzerland GDP for First Quarter (Mon 0900 CEST; Mon

0700 GMT; Mon 0300 EDT)

Consensus Forecast, Q/Q-Adjusted: 0.6%

Consensus Range, Q/Q-Adjusted: 0.5% to 0.7%

The consensus looks for growth at 0.6 percent on the

quarter, up from 0.5 percent in the flash.

Germany PMI Manufacturing Final for May (Mon 0955

CEST; Mon 0755 GMT; Mon 0355 EDT)

Consensus Forecast, Index: 49.9

Consensus Range, Index: 49.9 to 49.9

Manufacturing business expected to show slight contraction

at 49.9 in the May final reading, unrevised from 49.9 in the flash and down

from 51.4 in the April final.

Eurozone M3 Money Supply for April (Mon 1000 CEST; Mon

0800 GMT; Mon 0400 EDT)

Consensus Forecast, Y/Y-3-Month Moving Average: 3.1%

Consensus Range, Y/Y-3-Month Moving Average: 2.9% to 3.3%

The consensus forecasts money growth flat at 3.1 percent in

April versus 3.1 percent in March.

Eurozone PMI Manufacturing Final for May (Mon 1000

CEST; Mon 0800 GMT; Mon 0400 EDT)

Consensus Forecast, Index: 51.4

Consensus Range, Index: 51.4 to 51.4

Manufacturing business expected to show expansion at 51.4 in

the May final reading, unrevised from 51.4 in the flash and down from 52.2 in

the April final.

UK PMI Manufacturing Final for May (Mon 0930 BST; Mon

0830 GMT; Mon 0430 EDT)

Consensus Forecast, Index: 53.7

Consensus Range, Index: 53.7 to 53.7

Manufacturing business expected to show another month of expansion

at the same 53.7 in the May final reading, unrevised from 53.7 in the flash and

from 53.7 in the April final.

Eurozone Unemployment Rate for April (Mon 1100 CEST; Mon

0900 GMT; Mon 0500 EDT)

Consensus Forecast, Rate: 6.3%

Consensus Range, Rate: 6.2% to 6.3%

Joblessness is seen up a tick at 6.3 percent in April from

6.2 percent in March.

US PMI Manufacturing Final for May (Mon 0945 EDT; Mon

1345 GMT)

Consensus Forecast, Index: 55.3

Consensus Range, Index: 55.0 to 55.3

Manufacturing business expected to show robust expansion at 55.3

in the May final reading, unrevised from 55.3 in the flash and up from 54.5 in

the April final.

US ISM Manufacturing Index for May (Mon 1000 EDT; Mon

1400 GMT)

Consensus Forecast, Index: 53.1

Consensus Range, Index: 52.0 to 53.5

Forecasters expect the ISM report to show another month of nearly

steady growth at 53.1 in May after holding at 52.7 in April from March.

US Construction Spending for April (Mon 1000 EDT; Mon

1400 GMT)

Consensus Forecast, M/M: 0.3%

Consensus Range, M/M: 0.1% to 0.4%

The consensus looks for a solid increase of 0.3 percent in

April after a big 0.6 percent jump in March.

Tuesday

US Motor Vehicle Sales for May (ANYTIME)

Consensus Forecast, Total Vehicle Sales - Annual Rate: 16.0

M

Consensus Range, Total Vehicle Sales - Annual Rate: 15.7

M to 16.1 M

Sales expected pretty much flat at 16.0 million unit rate

from 15.9 million in April.

Eurozone HICP Flash for May (Tue 1100 CEST; Tue 0900

GMT; Tue 0500 EDT)

Consensus Forecast, HICP - Y/Y: 3.3%

Consensus Range, HICP - Y/Y: 3.0% to 3.4%

Consensus Forecast, Narrow Core - Y/Y: 2.4%

Consensus Range, Narrow Core - Y/Y: 2.3% to 2.5%

The energy price shock is seen raising Eurozone inflation to

3.3 percent in the May flash from 3.0 percent in the April final.

US JOLTS for April (Tue 1000 EDT; Tue 1400 GMT)

Consensus Forecast, Job Openings: 6.815 M

Consensus Range, Job Openings: 6.79 M to 6.89 M

Job openings expected down a bit at 6.815 million rate in

April from 6.866 million in March.

Wednesday

Australia GDP for First Quarter (Wed 1130 AEST; Wed 0130

GMT; Tue 2130 EDT)

Consensus Forecast, Q/Q: 0.5%

Consensus Range, Q/Q: 0.2% to 0.8%

Consensus Forecast, Y/Y: 2.6%

Consensus Range, Y/Y: 2.5% to 2.6%

The consensus sees growth slowing to 0.5 percent on quarter

in Q1 from 0.8 percent in Q4. Growth expected unchanged at 2.6 percent on year.

China PMI Services for May (Wed 0945 CST; Wed 0145

GMT; Tue 2145 EDT)

Consensus Forecast, Services Index: 52.2

Consensus Range, Services Index: 52.2 to 52.5

Services expected to expand at 52.2 in May versus 52.6 in

April.

France PMI Services Final for May (Wed 0850 CEST;

Wed 0650 GMT; Wed 0250 EDT)

Consensus Forecast, Services Index: 42.9

Consensus Range, Services Index: 42.9 to 42.9

The consensus sees no revision from the flash at 42.9, a

dismal recessionary reading, down from an already bad 46.5 in April.

Germany PMI Composite Final for May (Wed 0855

CEST; Wed 0655 GMT; Wed 0255 EDT)

Consensus Forecast, Composite Index: 48.6

Consensus Range, Composite Index: 48.6 to 48.6

Consensus Forecast, Services Index: 47.8

Consensus Range, Services Index: 47.8 to 47.8

No revisions expected from the flash at 48.6 for composite

and 47.8 for services, suggesting ongoing declines in business activity.

Eurozone PMI Composite Final for May (Wed 1000

CEST; Wed 0800 GMT; Wed 0400 EDT)

Consensus Forecast, Composite Index: 47.5

Consensus Range, Composite Index: 47.5 to 47.5

Consensus Forecast, Services Index: 46.4

Consensus Range, Services Index: 46.4 to 46.4

The consensus looks for the composite unrevised at 47.5 and

services at 46.4, very poor readings reflecting a big hit for the Eurozone from

the energy price shock.

UK PMI Composite Final for May (Wed 0930 BST; Wed 0830

GMT; Wed 0430 EDT)

Consensus Forecast, Composite Index: 48.5

Consensus Range, Composite Index: 48.5 to 48.5

Consensus Forecast, Services Index: 47.9

Consensus Range, Services Index: 47.9 to 47.9

No revisions expected from the flash at 48.5 for the

composite and 47.9 for services.

Eurozone PPI for April (Wed 1100 CEST; Wed 0900 GMT;

Wed 0500 EDT)

Consensus Forecast, M/M: 1.5%

Consensus Range, M/M: 0.7% to 0.9%

Consensus Forecast, Y/Y: 4.5%

Consensus Range, Y/Y: 2.8% to 6.3%

No more deflation in commodities with rising energy prices: PPI

is seen up 1.5 percent on the month and 4.5 percent from a year ago in April.

US ADP Employment Report for May (Wed 0815 EDT; Wed 1215

GMT)

Consensus Forecast, Private Payrolls - M/M: 118K

Consensus Range, Private Payrolls - M/M: 65K to 125K

Jobs expected up by a decent 118K in May after rising by

109K in April.

US PMI Composite Final for May (Wed 0945 EDT; Wed

1345 GMT)

Consensus Forecast, Composite Index: 51.7

Consensus Range, Composite Index: 51.7 to 51.7

Consensus Forecast, Services Index: 50.9

Consensus Range, Services Index: 50.9 to 50.9

The consensus sees composite unrevised at 51.7 and services

at 50.9 for the final May report.

US Factory Orders for April (Wed 1000 EDT; Wed 1400

GMT)

Consensus Forecast, M/M: 4.3%

Consensus Range, M/M: 0.3% to 5.5%

After aircraft lifted durable goods orders by a huge 7.9

percent for April, factory orders are expected up by 4.3 percent as factory

orders incorporates nondurables in addition to durables.

US ISM Services Index for May (Wed 1000 EDT; Wed 1400

GMT)

Consensus Forecast, Services Index: 53.7

Consensus Range, Services Index: 53.0 to 54.5

Services expected to show ongoing growth at 53.7 for May, nearly

flat from 53.6 in April. The Econoday services business activity index points

to a risk of a weaker number.

Thursday

Australia International Trade in Goods for April (Thu

1130 AEST; Thu 0130 GMT; Wed 2130 EDT)

Consensus Forecast, Balance: A$ 1.6 B

Consensus Range, Balance: -A$3.0 B to A$3.0 B

Rising commodity exports are seen helping to restore the

trade balance to a surplus of A$1.6 billion in April after a jump in imports

resulted in a A$1.8 billion deficit in March.

Eurozone Retail Sales for April (Thu 1100 CEST; Thu 0900

GMT; Thu 0500 EDT)

Consensus Forecast, M/M: -0.3%

Consensus Range, M/M: -0.6% to 0.0%

Consensus Forecast, Y/Y: 0.5%

Consensus Range, Y/Y: 0.1% to 0.7%

Sales seen down 0.3 percent on the month in April, a

miserable showing, and up only 0.5 percent on year.

US Jobless Claims for Week of May 30 (Thu 0830 EDT;

Thu 1230 GMT)

Consensus Forecast, Initial Claims - Level: 212 K

Consensus Range, Initial Claims - Level: 205 K to 218

K

Claims expected down to 212K from 215K last week, moving

back toward the 4-week moving average of 209K after rising 5K last week from

210K.

US Productivity and Costs for First Quarter (Thu 0830

EDT; Thu 1230 GMT)

Consensus Forecast, Nonfarm Productivity - Annual Rate:

0.8%

Consensus Range, Nonfarm Productivity - Annual Rate: 0.2%

to 0.8%

Consensus Forecast, Unit Labor Costs - Annual Rate: 2.3%

Consensus Range, Unit Labor Costs - Annual Rate: 1.9%

to 2.6%

Revised Q1 productivity and costs expected unchanged from

the preliminary report showing gains of 0.8 percent and 2.3 percent,

respectively.

Friday

Japan Household Spending for April (Fri 0830 JST; Thu

2330 GMT; Thu 1930 EDT)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: -0.5% to 1.2%

Consensus Forecast, Y/Y: -2.2%

Consensus Range, Y/Y: -2.7% to -1.1%

War in the Middle East are increasingly affecting consumer sentiment

and seen to be leading to a fifth straight month of declines in annual Japanese

real household spending in April.

Household expenditure for two or more people is seen falling

2.2 percent on the year in April after slipping 2.9 percent in March. On a

month-on-month basis, household spending is expected to rise 0.2 percent in

April after falling 1.3 percent in March.

India Reserve Bank of India Announcement (ANYTIME)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 5.25%

Consensus Range, Level: 5.25% to 5.25%

RBI expected to keep rates unchanged but to anticipate rate

increases if inflation does not ease.

France Industrial Production for April (Fri 0845

CEST; Fri 0645 GMT; Fri 0245 EDT)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: -0.2% to 0.2%

Output expected to show 0.2 percent increase in April from

March after rising 1.0 percent in March from February.

Eurozone GDP for First Quarter (Fri 1100 CEST; Fri 0900

GMT; Fri 0500 EDT)

Consensus Forecast, Q/Q: 0.1%

Consensus Range, Q/Q: 0.1% to 0.1%

Consensus Forecast, Y/Y: 0.8%

Consensus Range, Y/Y: 0.5% to 0.8%

The consensus sees no revision in the final from the last

report showing slow growth at 0.1 percent on quarter and 0.8 percent on year.

Canada Labour Force Survey for May (Fri 0830 EDT; Fri

1230 GMT)

Consensus Forecast, Employment - M/M: 10

Consensus Range, Employment - M/M: 8 to 25

Consensus Forecast, Unemployment Rate: 6.9%

Consensus Range, Unemployment Rate: 6.8% to 6.9%

Employment expected to rise an unimpressive 10K in May after

declining 18K in April. Jobless rate seen flat at 6.9 percent.

US Employment Situation for May (Fri 0830 EDT; Fri

1230 GMT)

Consensus Forecast, Nonfarm Payrolls - M/M: 85K

Consensus Range, Nonfarm Payrolls - M/M: 50K to 105K

Consensus Forecast, Unemployment Rate: 4.3%

Consensus Range, Unemployment Rate: 4.3% to 4.4%

Consensus Forecast, Private Payrolls - M/M: 90K

Consensus Range, Private Payrolls - M/M: 40K to 120K

Consensus Forecast, Manufacturing Payrolls - M/M: 1K

Consensus Range, Manufacturing Payrolls - M/M: -2K to

4K

Consensus Forecast, Average Hourly Earnings - M/M: 0.3%

Consensus Range, Average Hourly Earnings - M/M: 0.2%

to 0.3%

Consensus Forecast, Average Hourly Earnings - Y/Y: 3.4%

Consensus Range, Average Hourly Earnings - Y/Y: 3.4%

to 3.5%

Consensus Forecast, Average Workweek: 34.3

Consensus Range, Average Workweek: 34.3 to 34.3

The consensus sees another decent increase of 85K jobs in

May after 115K in April. The jobless rate is expected flat at 4.3 percent.

US Consumer Credit for April (Fri 1500 EDT; Fri 1900

GMT)

Consensus Forecast, M/M: $17.0 B

Consensus Range, M/M: $8.4 B to $18.0 B

Credit expected up $17.0 billion on the month for April

after rising a strong $25 billion in March.

|