|

The Week Ahead: Highlights

US Preview

Fed's Warsh, FOMC in Focus as Inflation Heats Up

By Theresa Sheehan, Econoday Economist

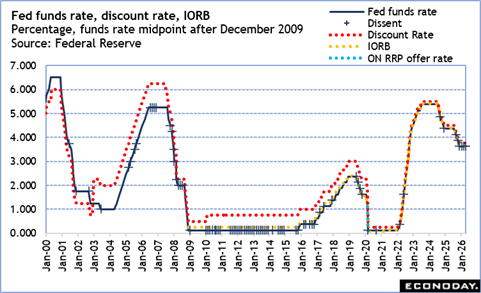

The big event of the June 15 week is the Tuesday-Wednesday

FOMC meeting, the first to be chaired by Kevin Warsh less than a month after

being sworn in as a governor and Fed chair.

Expectations call for no change in the federal funds target

rate range of 3.50-3.75 percent. However, sentiment among more than a few of

the 19 FOMC participants is turning more hawkish about inflation. It is

possible that there will be sufficient concern about the recent heating up in

the inflation indicators that a majority could want a 25-basis point increase

as a mid-cycle adjustment to ensure that inflation does not get entrenched and

to return to downward trend disrupted by the war on Iran.

The FOMC meeting statement and summary of economic

projections is expected at 14:00 ET on Wednesday followed by the chair's press

conference at 14:30 ET.

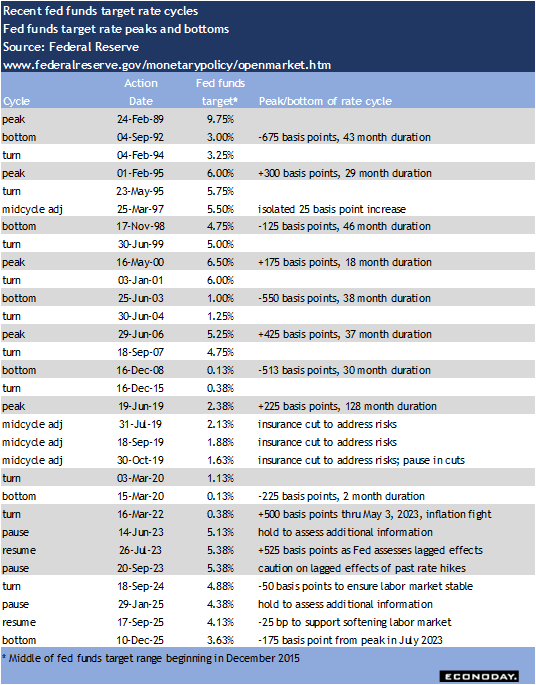

There has not been an FOMC meeting without at least one

dissent in the vote since June 2025. This illustrates policymakers' dilemma of

trying to balance the dual mandate between a lackluster labor market and

stubborn inflation. The economic data has been on a thorny path between

achieving maximum employment and price stability as the economy adjusts to

economic shocks from harsh new tariffs, a prolonged federal government

shutdown, lately from war, and over a year of a chaotic geopolitical

environment. The resilience of the economy at least in a few robust sectors

-- has kept the US out of recession. Monetary policy has remained cautious and

reluctant to adjust without clear signals from the data. Achieving unanimity

among policymakers has been difficult across the spectrum of interpreting the

data. The June meeting will not be an exception.

At his post-meeting press briefing on March 18, then-Chair

Jerome Powell quipped that if the FOMC were to skip issuing a summary of

economic projections (SEP), that would have been the meeting. The June meeting

would normally see the next update of the forecasts. New Chair Warsh is known

to dislike the SEP. It is not impossible that given the even more uncertain

conditions than existed at the March 17-18 meeting, he could determine that it

is inappropriate at this time, perhaps with an eye to later ending the

publication entirely. There could be more about this when the minutes of the

meeting are released on Wednesday, July 8 at 14:00 ET.

The June meeting is also the one at which policymakers lay

the groundwork for the Fed's report to Congress and the chair's semiannual

monetary policy testimony. The Senate Banking Committee and the House

Financial Services Committee are likely to be as anxious to schedule Warsh's

appearance later in June or early in July as they were reluctant to bring

Powell before the respective committees back in the winter months. The winter

semiannual testimony never took place.

Warsh has plans to change how the Fed approaches setting

monetary policy and communicating it with the public. Warsh could well use the

post-meeting press briefing to set the stage for those future changes as he

takes questions from a press corps that is skeptical about his commitment to an

independent central bank. Warsh's decision to hire consultants associated with

Project 2025 is worrisome about a political agenda infiltrating the Fed to an

uncomfortable degree.

The Week Ahead: Econoday Consensus Forecasts

Monday

Eurozone Industrial Production for April (Mon 1100

CEST; Mon 0900 GMT; Mon 0500 EDT)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: 0.1% to 0.5%

Consensus Forecast, Y/Y: 0.3%

Consensus Range, Y/Y: 0.2% to 0.5%

Output expected up 0.2 percent on month and up 0.3 percent

on year in April after rising 0.2 percent on month and decreasing 2.1 percent

on year in March.

Canada Housing Starts for May (Mon 0815 EDT; Mon 1215

GMT)

Consensus Forecast, Annual Rate: 257,500

Consensus Range, Annual Rate: 243,000 to 260,000

Canada Manufacturing Sales for April (Mon 0830 EDT;

Mon 1230 GMT)

Consensus Forecast, M/M: 4.6%

Consensus Range, M/M: 4.0% to 4.6%

The consensus agrees with the Stats Canada preliminary

forecast calling for a big 4.6 percent increase in April after increasing 3.0

percent in March.

US Empire State Manufacturing Index for June (Mon

0830 EDT; Mon 1230 GMT)

Consensus Forecast, Index: 12.5

Consensus Range, Index: 9.0 to 16.0

The consensus looks for the manufacturing business index at 12.5

in June versus 19.6 in May. That would suggest somewhat slower expansion in

business activity relative to May.

US Industrial Production for May (Mon 0915 EDT; Mon 1315

GMT)

Consensus Forecast, Industrial Production - M/M: 0.2%

Consensus Range, Industrial Production - M/M: 0.0% to

0.5%

Consensus Forecast, Manufacturing Output - M/M: 0.3%

Consensus Range, Manufacturing Output - M/M: 0.3% to

0.3%

Consensus Forecast, Capacity Utilization Rate: 76.2%

Consensus Range, Capacity Utilization Rate: 76.0% to

76.3%

Forecasters see modest increases of 0.2 percent for

industrial output and 0.3 percent for manufacturing in May. Business equipment

spending as part of the AI boom continues to underpin output.

US Housing Market Index for June (Mon 1000 EDT; Mon

1400 GMT)

Consensus Forecast, Index: 36

Consensus Range, Index: 36 to 37

The consensus sees builder sentiment down at 36 June from an

already pessimistic 37 in May.

Tuesday

China Fixed Asset Investment for May (Tue 1000 CST; Tue

0200 GMT; Mon 2200 EDT)

Consensus Forecast, Year to Date on Y/Y Basis: -2.3%

Consensus Range, Year to Date on Y/Y Basis: -2.8% to -0.8%

Still shocking to see ongoing contraction in what used to be

China's strength. Forecasters see FAI down 2.3 percent on year again in May

after decreasing 2.36 percent in April.

China Industrial Production for May (Tue 1000 CST; Tue

0200 GMT; Mon 2200 EDT)

Consensus Forecast, Y/Y: 4.3%

Consensus Range, Y/Y: 4.3% to 4.7%

The consensus looks for output up 4.3 percent on year in May

after rising 4.1 percent in April, still unimpressive.

China Retail Sales for May (Tue 1000 CST; Tue 0200

GMT; Mon 2200 EDT)

Consensus Forecast, Y/Y: -0.3%

Consensus Range, Y/Y: -0.9% to 0.8%

Another bleak report expected to show sales down 0.3 percent

on year in May after rising only 0.2 percent in April on the year.

Japan Bank of Japan Announcement (Tue 1130 JST; Tue 0230

GMT; Mon 2230 EDT)

Consensus Forecast, Change: 25 bp

Consensus Range, Change: 25 bp to 25 bp

Consensus Forecast, Level: 1.00 %

Consensus Range, Level: 1.00 % to 1.00 %

The Bank of Japan is expected to raise the target for the

overnight interest rate to 1.00 percent from 0.75 percent in a unanimous or

majority vote amid growing upside risks to inflation triggered by the Mideast

conflict. Governor Kazuo Ueda, who hinted at an imminent rate hike in a recent

speech, will miss the meeting for medical treatment. It would be the bank's

first rate hike since December, when the board unanimously decided to raise the

policy rate by 25 basis points to a 30-year high after standing pat for nearly

a year.

Australia RBA Announcement (Tue 1430 AEST; Tue 0430

GMT; Tue 1230 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 4.35%

Consensus Range, Level: 4.35% to 4.35%

Forecasters believe the RBA bought itself time with past

rate increases to hold steady this time even if inflation is way too hot. With

inflation running above target, the expectation calls for more rate hikes soon,

just not this time.

Italy CPI for May (Tue 1000 CEST; Tue 0800 GMT; Tue

0400 EDT)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: 0.4% to 0.4%

Consensus Forecast, Y/Y: 3.2%

Consensus Range, Y/Y: 3.2% to 3.2%

The consensus sees no revision from the flash to the final

with increases of 0.4 percent on month and 3.2 percent on year for May.

Germany ZEW Survey for June (Tue 1100 CEST; Tue 0900

GMT; Tue 0500 EDT)

Consensus Forecast, Current Conditions: -77.5

Consensus Range, Current Conditions: -81.0 to -77.0

Consensus Forecast, Economic Sentiment: -6.5

Consensus Range, Economic Sentiment: -16.0 to 0

Current conditions seen nearly flat at minus 77.5 in June but

sentiment seen improving to minus 6.5 from minus 10.2.

US Housing Starts and Permits for May (Tue 0830 EDT;

Tue 1230 GMT)

Consensus Forecast, Starts - Annual Rate: 1.430 M

Consensus Range, Starts - Annual Rate: 1.374 M to 1.472

M

Consensus Forecast, Permits - Annual Rate: 1.427 M

Consensus Range, Permits - Annual Rate: 1. 396 M to 1.460

M

Rising mortgage rates and consumer caution expected to

dampen sales to a 1.430 million unit rate in May from 1.465 million in April.

US Imports and Export Prices for May (Tue 0830 EDT;

Tue 1230 GMT)

Consensus Forecast, Import Prices - M/M: 1.3%

Consensus Range, Import Prices - M/M: 0.8% to 1.5%

Consensus Forecast, Export Prices - M/M: 2.0%

Consensus Range, Export Prices - M/M: 0.3% to 2.1%

Higher energy costs seen lifting import prices by 1.3

percent and export prices by a whopping 2.0 percent on the month in May.

Wednesday

Japan Merchandise Trade for May (Wed 0850 JST; Tue

2350 GMT; Tue 1950 EDT)

Consensus Forecast, Balance: -559.60 B

Consensus Range, Balance: -660.00 B to -348.70 B

Consensus Forecast, Imports - Y/Y: 12.5%

Consensus Range, Imports - Y/Y: 9.9% to 16.6%

Consensus Forecast, Exports - Y/Y: 14.8%

Consensus Range, Exports - Y/Y: 10.7% to 19.0%

Driven by increasing imports amid prolonged tensions in the

Middle East and the weak yen, Japan's trade balance is expected to fall into

deficit for the first time in four months in May. Robust trade activity is

expected to lift export values from a year earlier for the ninth consecutive

month and import values for the fourth straight month.

Japanese exports are expected to rise14.8 percent, the same

as in April. The April value reached the second-highest level on record at

10.5 trillion, led by double-digit percentage gains in shipments of computer

chips, non-ferrous metals and engines.

As geopolitical uncertainty persists amid concerns over a

blockage of the Strait of Hormuz, resource-poor Japan has been scrambling to

diversify its imports of natural resources away from the Middle East. Coupled

with the ongoing weakness of the yen, import values are expected to rise 12.5

percent in May after a revised 9.8 percent increase in April from the initially

9.7 percent.

Japan's customs-cleared trade balance is expected to fall

into deficit for the first time in four months in May, with the trade balance

seen posting a deficit of 559.60 billion yen after a revised surplus of 299.27

billion yen in the previous month.

Japan Machinery Orders for April (Wed 0850 JST; Tue

2350 GMT; Tue 1950 EDT)

Consensus Forecast, M/M: -0.3%

Consensus Range, M/M: -2.0% to 6.5%

Consensus Forecast, Y/Y: 9.9%

Consensus Range, Y/Y: 8.5% to 17.4%

Japan's core machinery orders, a leading indicator of

business investment in equipment and software, are expected to edge down on the

month in April while extending their year-on-year gains to a fifth consecutive

month as corporate appetite for capital spending remained resilient despite

geopolitical uncertainty stemming from war in the Middle East.

Capital investment related to semiconductors is expected to

remain active in April amid growing expectations of expanding demand for

artificial intelligence technologies. Machine tool orders also posted a sharp

increase during the month, providing support for core machinery orders.

Core machinery orders are seen falling 0.3 percent on the

month in April after falling 9.4 percent a month earlier. The March decline

partly reflected a payback from the 13.6 percent surge recorded in February,

when one-off large-ticket deals boosted orders. On a year-over-year basis, core

machinery orders are expected to rise 9.9 percent in April after increasing 5.9

percent in March.

UK CPI for May (Wed 0700 BST; Wed 0600 GMT; Wed 0200

EDT)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: 0.3% to 0.5%

Consensus Forecast, Y/Y: 3.1%

Consensus Range, Y/Y: 3.0% to 3.2%

The consensus sees inflation bouncing back to 3.1 percent on

year after falling more than expected to 2.8 percent in April.

Sweden Riksbank Policy Announcement (Wed 0730 GMT;

Wed 0330 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Policy Rate - Target Rate: 1.75%

Consensus Range, Policy Rate - Target Rate: 1.75% to

1.75%

Forecasters see a hawkish hold on rates with an increase in

the Riksbank inflation forecast and a higher projected rate path.

Eurozone HICP for May (Wed 1100 CEST; Wed 0900 GMT; Wed

0500 EDT)

Consensus Forecast, HICP - Y/Y: 3.2%

Consensus Range, HICP - Y/Y: 3.2% to 3.2%

Consensus Forecast, Narrow Core - Y/Y: 2.5%

Consensus Range, Narrow Core - Y/Y: 2.5% to 2.5%

The consensus anticipates no revision from the HICP flash at

3.2 percent and 2.5 percent for core from year ago.

US Retail Sales for May (Wed 0830 EDT; Wed 1230 GMT)

Consensus Forecast, Retail Sales - M/M: 0.5%

Consensus Range, Retail Sales - M/M: 0.2% to 0.8%

Consensus Forecast, Ex-Vehicles - M/M: 0.5%

Consensus Range, Ex-Vehicles - M/M: 0.3% to 0.8%

Consensus Forecast, Ex-Vehicles & Gas - M/M: 0.3%

Consensus Range, Ex-Vehicles & Gas - M/M: -0.1%

to 0.5%

Spending looks robust with support from rising goods prices

and auto sales. The consensus sees retail sales up 0.5 percent for a second

straight month.

US Business Inventories for April (Wed 1000 EDT; Wed

1400 GMT)

Consensus Forecast, M/M: 0.5%

Consensus Range, M/M: 0.3% to 0.7%

A strong 0.5 percent increase is expected for April after a

big 0.9 percent in March.

US Pending Home Sales Index for May (Wed 1000 EDT;

Wed 1400 GMT)

Consensus Forecast, M/M: 0.9%

Consensus Range, M/M: -0.1% to 1.5%

Another robust rise in pending home sales, 0.9 percent, is

expected for May after the 1.0 percent increase in April.

US FOMC Announcement (Wed 1400 EDT; Wed 1800 GMT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Federal Funds - Target Range: 3.50%

to 3.75%

Consensus Range, Federal Funds Rate - Target Rate: 3.50%

to 3.75% to 3.50% to 3.75%

Forecasters see no interest rate change or immediate shift

in balance sheet policy. The consensus does look for the Fed to shift its current

easing bias toward a more neutral stance. That means policymakers are saying

the next step could equally be easing or tightening. Such a hawkish shift from

the first FOMC meeting of Kevin Warsh's tenure is not what President Trump

bargained for when he named Warsh as chair but there is an emerging majority on

the FOMC looking for a tougher stance on inflation.

Brazil Selic Rate for June (Wed 0630 BRT; Wed 0930

GMT; Wed 0530 EDT)

Consensus Forecast, Level: 14.25%

Consensus Range, Level: 14.25% to 14.50%

Consensus Forecast, Change: -25 bp

Consensus Range, Change: -25 bp to 0 bp

Forecasters look for a third straight rate cut in June after

cuts in March and April but they are scaling back expectations for more rate

cuts after that. They note policymakers are warning that demand-driven core

inflation appears to be heating up as President Lula cranks up the stimulus,

and some say it's already time for a pause.

Thursday

New Zealand GDP for First Quarter (Thu 1045 NZDT; Wed

2245 GMT; Wed 1845 EDT)

Consensus Forecast, Q/Q: 0.8%

Consensus Range, Q/Q: 0.7% to 1.0%

Consensus Forecast, Y/Y: 1.0%

Consensus Range, Y/Y: 0.9% to 1.1%

GDP expected to show the economy was picking up steam in Q1

before the energy price shock with the Q/Q increase expected at 0.8 percent, up

from 0.2 percent in Q4.

Taiwan Central Bank of the Republic of China for Second Quarter

(ANYTIME)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 2.0%

Consensus Range, Level: 2.0% to 2.0%

The consensus sees the bank on hold for now but likely to

raise rates later if inflation does not cool.

Switzerland SNB Monetary Policy Assessment for June (Thu

0930 CEST; Thu 0730 GMT; Thu 0330 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 0.0%

Consensus Range, Level: 0.0% to 0.0%

No change is the call.

Norway Norges Bank Rate Decision for June (Thu 1000

CEST; Thu 0800 GMT; Thu 0400 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 4.25%

Consensus Range, Level: 4.25% to 4.25%

After raising rates last month, the bank has room to hold

steady this month to see how inflation develops.

UK BoE Announcement & Minutes (Thu 1200 BST; Thu

1100 GMT; Thu 0700 EDT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 3.75%

Consensus Range, Level: 3.75% to 3.75%

Forecasters see the bank on hold for a fourth straight time

with seven MPC members supporting no change and two supporting a rate increase.

US Jobless Claims for Week of June 13 (Thu 0830 EDT;

Thu 1230 GMT)

Consensus Forecast, Initial Claims - Level: 225K

Consensus Range, Initial Claims - Level: 220K to 228K

Forecasters expect claims to recede to 225K after rising by

4K to 229K last week.

US Philadelphia Fed Manufacturing Index for June (Thu

0830 EDT; Thu 1230 GMT)

Consensus Forecast, Index: 11.0

Consensus Range, Index: 5.0 to 12.0

The consensus sees better growth with the index at 11.0 in

June, up from minus 0.4 in May.

US Leading Indicators for May (Thu 1000 EDT; Thu 1400

GMT)

Consensus Forecast, M/M: 0.1%

Consensus Range, M/M: -0.1% to 0.2%

A marginal 0.1 percent increase is the call.

Friday

Japan CPI for May (Fri 0830 JST; Thu 2330 GMT; Thu 1930

EDT)

Consensus Forecast, CPI - Y/Y: 1.5%

Consensus Range, CPI - Y/Y: 1.4% to 1.6%

Consensus Forecast, Ex-Fresh Food - Y/Y: 1.4%

Consensus Range, Ex-Fresh Food - Y/Y: 1.4% to 1.5%

Consensus Forecast, Ex-Fresh Food & Energy - Y/Y:

1.9%

Consensus Range, Ex-Fresh Food & Energy - Y/Y: 1.7%

to 2.0%

Japan's nationwide core consumer price index, which excludes

fresh food, is expected to be little changed on the year in May, but is likely

to remain below the Bank of Japan's 2 percent inflation target for a fourth

consecutive month.

Mirroring the trend seen in the Tokyo CPI released on May

29, consumer inflation continued to decelerate amid slower food price growth

and the effects of government gasoline subsidies. In addition, the Tokyo

government's policy of waiving basic water service charges during the summer,

starting in May, as well as reductions in early childcare costs, including

nursery school fees, contributed to a further easing in inflation.

These measures have helped restrain inflationary pressures

even as geopolitical tensions in the Middle East have pushed up international

oil and other commodity prices. The tensions have also weighed on the yen,

raising import costs and creating upward pressure on domestic prices.

The core CPI is expected to be unchanged at a 1.4 percent

rise on the year in May, while the overall CPI is forecast to rise 1.5 percent

after increasing 1.4 percent in April. Core-core CPI, which excludes both fresh

food and energy, is also expected to remain unchanged, rising 1.9 percent from

a year earlier in May.

Germany PPI for May (Wed 0800 CEST; Wed 0600 GMT; Wed

0200 EDT)

Consensus Forecast, M/M: 0.6%

Consensus Range, M/M: 0.2% to 2.0%

Consensus Forecast, Y/Y: 2.5%

Consensus Range, Y/Y: 2.0% to 2.5%

Wholesale prices expected to reflect the impact of rising

energy costs. PPI seen up 0.6 percent on the month and 2.5 percent on year in

May.

Canada Retail Sales for April (Fri 0830 EDT; Fri 1230

GMT)

Consensus Forecast, M/M: 0.6%

Consensus Range, M/M: 0.5% to 0.6%

Forecasters agree, as usual, with Statistics Canada's

preliminary forecast calling for an increase of 0.6 percent in nominal terms for

April from March, presumably with a boost from rising fuel prices.

|