|

The Week Ahead: Highlights

Asia-Pacific Preview

China GDP, Monthly Activity Reports in Focus

By Brian Jackson, Econoday Economist

Chinas quarterly GDP release and monthly activity data for

June will be the main focus in the Asia-Pacific region in the week ahead. GDP

recorded solid growth early in the year, but next weeks report will likely

reflect the impact of the Iran conflict to a greater degree, with monthly data

showing weakness in both April and May. PMI survey data for June showed subdued

conditions in both the manufacturing and services sector, suggesting that the

monthly data next week may fail to show a strong improvement. Next weeks data

will also be accompanied by officals updated assessment of conditions and

policy settings.

The Bank of Koreas policy meeting is also scheduled, with a

rate increase seen as likely. Officials there have kept rates on hold since

mid-2025, but two of the seven policy board members voted for a rate hike at

the most recent meeting in late May. Speaking after the meeting, new BoK

Governor Shin Hyan Song advised then that he expected policy rates to rise in

coming months, citing an upward revision to inflation forecasts in response to

the Iran conflict.

Elsewhere in the region, India reports inflation and trade

data, while Singapore will publish GDP and trade data. Australian consumer and

business confidence surveys will be watched for evidence that recent tax

changes by the government and policy rate increases by the Reserve Bank of

Australia are having an impact on sentiment.

US Preview

Feds Warsh Set for Monetary Policy Testimony; CPI/PPI

Due

By Theresa Sheehan, Econoday Economist

Economic data in the July 13 week will be a backdrop for the

semiannual monetary policy testimony of newly installed Fed Chair Kevin Warsh

before the House Financial Services Committee at 10:00 ET on Tuesday and the

Senate Banking Committee at 10:00 ET on Wednesday. Amid the political turmoil

of earlier this year, former Chair Jerome Powell was never scheduled to give

the normal winter testimony and there was no monetary policy report to Congress

issued. This July will see the monetary policy report out on July 10.

The testimony is ostensibly intended to focus on monetary

policy. Warshs opening remarks will meet that goal. However, given that this

is the last real chance for members of the respective committees to get on the

record regarding their views on the Fed and its conduct before the midterms,

questions about monetary policy will be dealt with in relatively short orders.

Instead, Warsh will have ample opportunity to highlight his plans for reform at

the central bank, make clear his intentions for maintaining central bank

independence, and avoid leading questions on fiscal policy. Committee members

will have a chance to voice their skepticism about Warshs ability to remain

above politics in setting policy, ask who he plans to appoint to the five

working groups to shape reforms at the Fed, and demand to know which private

data he will be introducing as a guide to monetary policy.

The Fed announced the leadership of the five task forces on

July 9

(https://www.federalreserve.gov/newsevents/pressreleases/monetary20260709a.htm).

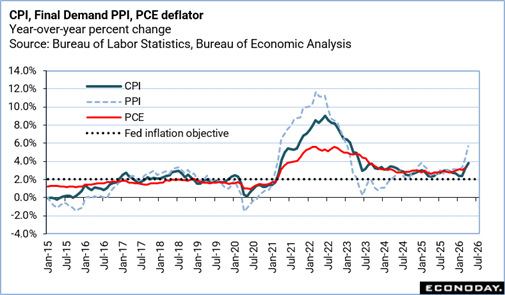

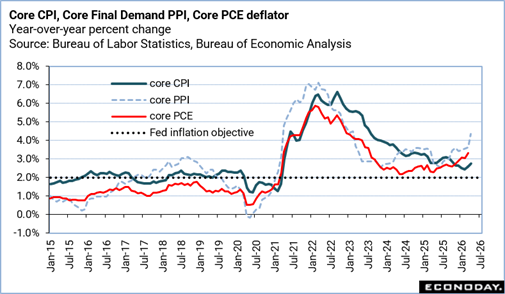

The big data for the week will be the inflation data for

June with the consumer price index (CPI) at 8:30 ET on Tuesday, the

final-demand producer price index (PPI) at 8:30 ET on Wednesday, and the import

and export price indexes at 8:30 ET on Friday. All three are expected to

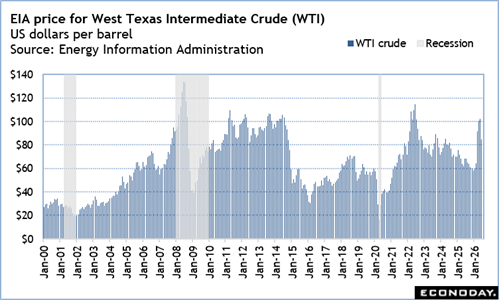

reflect easing oil prices generally, and gasoline in particular. Energy prices

remain elevated compared to a year ago. If upward price pressure was less in

June, it is keeping inflation above the Feds 2 percent objective. The present

renewed increase in oil prices means that that relief is going to be

short-lived. Consumers and producers will get another round of higher prices

passing into the supply chain in July and August. Fed policymakers are going to

have to lean hawkish on inflation when the meet on July 28-29.

The Week Ahead: Econoday Consensus Forecasts

Monday

India CPI for June (Mon 1600 IST; Mon 1030 GMT; Mon 0630

EDT)

Consensus Forecast, Y/Y: 4.15%

Consensus Range, Y/Y: 3.80% to 4.21%

Annual CPI expected up to 4.15 percent in June from 3.93

percent in May, reflecting rising energy costs.

Tuesday

China Merchandise Trade for June (ANYTIME)

Consensus Forecast, Balance of Trade: $121.0 B

Consensus Range, Balance of Trade: $110 B to $123.9

Consensus Forecast, Imports - Y/Y: 25.0%

Consensus Range, Imports - Y/Y: 24.0% to 27.3%

Consensus Forecast, Exports - Y/Y: 18.8%

Consensus Range, Exports - Y/Y: 17.5% to 20.9%

The trade surplus expected to surge to $121.0 billion in

June from $105.43 billion in May as exports maintain their momentum.

US NFIB Small Business Optimism Index for June (Tue

0600 EDT; Tue 1000 GMT)

Consensus Forecast, Index: 95.6

Consensus Range, Index: 95.0 to 96.0

Business sentiment expected essentially flat at 95.6 in June

from 95.3 in May.

US CPI for June (Tue 0830 EDT; Tue 1230 GMT)

Consensus Forecast, CPI - M/M: -0.1%

Consensus Range, CPI - M/M: -0.3% to 0.0%

Consensus Forecast, CPI - Y/Y: 3.8%

Consensus Range, CPI - Y/Y: 3.7% to 4.0%

Consensus Forecast, Ex-Food & Energy - M/M: 0.2%

Consensus Range, Ex-Food & Energy - M/M: 0.2% to 0.3%

Consensus Forecast, Ex-Food & Energy - Y/Y: 2.9%

Consensus Range, Ex-Food & Energy - Y/Y: 2.8% to 2.9%

Falling gas prices on the month should depress the monthly

figure to show a decline of 0.1 percent with the year-year at 3.8 percent

versus 4.2 percent in May. Core seen up 0.2 percent and 2.9 percent,

respectively. If not for the rebound in energy prices in the last few days,

these might have been reassuring numbers for the markets and the Fed.

Wednesday

Japan Machinery Orders for May (Wed 0850 JST; Tue

2350 GMT; Tue 1950 EDT)

Consensus Forecast, M/M: -5.0%

Consensus Range, M/M: -6.5% to -0.7%

Consensus Forecast, Y/Y: 13.7%

Consensus Range, Y/Y: 12.2% to 16.6%

Japans core machinery orders, a key leading indicator of

business investment in equipment and software, are expected to decline on the

month in May after unexpectedly rising a month earlier. The decline is likely

to reflect a reactionary pullback following Aprils sharp increase, when orders

from industries including shipbuilding surged.

Core machinery orders are projected to fall 5.0 percent on

the month in May after rising 8.7 percent in April, supported by solid gains in

computer orders. The Cabinet Office also maintained its assessment that

machinery orders are showing signs of a pickup.

Capital spending is expected to remain resilient, supported

by expectations of expanding demand for artificial intelligence technologies,

with annual core machinery orders seen rising 13.7 percent in May after gaining

15.6 percent in April, expected to mark a sixth straight month of year-on-year

growth.

China Fixed Asset Investment for June (Wed 1000 CST; Wed

0200 GMT; Tue 2200 EDT)

Consensus Forecast, Year to Date on Y/Y Basis: -4.9%

Consensus Range, Year to Date on Y/Y Basis: -5.2% to -4.6%

Still hard to get used to big declines in an indicator that

was always so robust: the consensus looks for minus 4.9 percent for June, even

weaker than the minus 4.1 percent in May.

China GDP for Second Quarter (Wed 1000 CST; Wed 0200

GMT; Tue 2200 EDT)

Consensus Forecast, Q/Q: 0.9%

Consensus Range, Q/Q: 0.8% to 1.0%

Consensus Forecast, Y/Y: 4.5%

Consensus Range, Y/Y: 4.4% to 4.8%

Annual GDP growth expected down to 4.5 percent on year in Q2

versus 5.0 percent in Q1.

China Industrial Production for June (Wed 1000 CST; Wed

0200 GMT; Tue 2200 EDT)

Consensus Forecast, Y/Y: 4.6%

Consensus Range, Y/Y: 4.5% to 5.0%

Output seen up 4.6 percent on year in June versus 4.5

percent in May.

China Retail Sales for June (Wed 1000 CST; Wed 0200

GMT; Tue 2200 EDT)

Consensus Forecast, Y/Y: -0.1%

Consensus Range, Y/Y: -0.2% to 0.4%

Sales seen down 0.1 percent on year in June after declining

0.6 percent in May.

Eurozone Industrial Production for May (Wed 1100 CEST;

Wed 0900 GMT; Wed 0500 EDT)

Consensus Forecast, M/M: 0.3%

Consensus Range, M/M: -0.1% to 0.8%

Consensus Forecast, Y/Y: -0.4%

Consensus Range, Y/Y: -0.4% to 0.2%

Output expected up by 0.3 percent on the month in May after a

0.1 percent increase in April.

US PPI-Final Demand for June (Wed 0830 EDT; Wed 1230

GMT)

Consensus Forecast, PPI-FD - M/M: -0.1%

Consensus Range, PPI-FD - M/M: -0.3% to 0.6%

Consensus Forecast, PPI - Y/Y: 6.2%

Consensus Range, PPI - Y/Y: 6.1% to 6.6%

Consensus Forecast, Ex-Food & Energy - M/M: 0.4%

Consensus Range, Ex-Food & Energy - M/M: 0.1% to 0.5%

Consensus Forecast, Ex-Food & Energy - Y/Y: 5.2%

Consensus Range, Ex-Food & Energy - Y/Y: 4.9% to 5.2%

Consensus Forecast, Ex-Food, Energy, Trade Svcs - M/M:

0.4%

Consensus Range, Ex-Food & Energy, Trade Svcs - M/M:

0.3% to 0.4%

Producer prices seen down 0.1 percent on the month on

falling energy prices. On year, its expected up 6.2 percent.

Canada Manufacturing Sales for May (Wed 0830 EDT; Wed

1230 GMT)

Consensus Forecast, M/M: 1.1%

Consensus Range, M/M: 1.1% to 1.1%

The consensus agrees with the Stats Canada preliminary

estimate of up 1.1 percent for May from April.

US Empire State Manufacturing Index for July (Wed

0830 EDT; Wed 1230 GMT)

Consensus Forecast, Index: 8.6

Consensus Range, Index: 4.0 to 11.5

The manufacturing index is expected to show slightly faster

expansion at 8.6 in July versus 5.7 in June.

Canada Bank of Canada Announcement (Wed 0945 EDT; Wed

1245 GMT)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 25 bp

Consensus Forecast, Level: 2.25%

Consensus Range, Level: 2.25% to 2.50%

The consensus sees the bank on hold in light of mixed

showing for employment with inflation not as bad as feared.

Thursday

South Korea Bank of Korea Announcement (Thu 1000 KST;

Thu 0100 GMT; Wed 2100 EDT)

Consensus Forecast, Change: 25 bp

Consensus Range, Change: 25 bp to 25bp

Consensus Forecast, Level: 2.75%

Consensus Range, Level: 2.75% to 2.75%

The BOK is expected to raise rates by 25 bp to deal with

rising imported input cost pressure on inflation.

UK Monthly GDP for May (Thu 0700 BST; Thu 0600 GMT;

Thu 0200 EDT)

Consensus Forecast, M/M: 0.1%

Consensus Range, M/M: 0.1% to 0.1%

A very modest 0.1 percent increase is the call after a

decrease of 0.1 percent in the previous month.

UK Industrial Production for May (Thu 0700 BST; Thu

0600 GMT; Thu 0200 EDT)

Consensus Forecast, Industrial Production - M/M: 0.1%

Consensus Range, Industrial Production - M/M: -0.1%

to 0.2%

Consensus Forecast, Industrial Production - Y/Y: 1.2%

Consensus Range, Industrial Production - Y/Y: -0.1%

to 1.3%

Consensus Forecast, Manufacturing Production - M/M: -0.1%

Consensus Range, Manufacturing Production - M/M: -0.3%

to 0.2%

Consensus Forecast, Manufacturing Production - Y/Y: 2.0%

Consensus Range, Manufacturing Production - Y/Y: -0.1%

to 2.4%

The consensus looks for industrial output up 0.1 percent on

the month and up 1.2 percent on year in May.

Italy CPI for June (Thu 1000 CEST; Thu 0800

GMT; Thu 0400 EDT)

Consensus Forecast, M/M: 0.0%

Consensus Range, M/M: 0.0% to 0.1%

Consensus Forecast, Y/Y: 3.0%

Consensus Range, Y/Y: 3.0% to 3.1%

Forecasters expect no revision in the final report from the

flash at 0.0 percent on month and 3.0 percent on year.

Eurozone Merchandise Trade for May (Thu 1100 CEST; Thu

0900 GMT; Thu 0500 EDT)

Consensus Forecast, Balance: E2.5 B

Consensus Range, Balance: E1.0 B to E6.5 B

The surplus is expected to widen to E2.5 billion from E1.3

billion a month earlier.

Canada Housing Starts for June (Thu 0815 EDT; Thu 1215

GMT)

Consensus Forecast, Annual Rate: 260K

Consensus Range, Annual Rate: 220K to 270K

Starts expected essentially unchanged at a 260K rate in June

from 261K in May.

US Jobless Claims for Week of July 16 (Thu 0830 EDT;

Thu 1230 GMT)

Consensus Forecast, Initial Claims - Level: 220K

Consensus Range, Initial Claims - Level: 216K to 225K

Claims expected at 220K, up from 215K last week, very close

to the latest 4-week moving average at 218.75K.

US Retail Sales for June (Thu 0830 EDT; Thu 1230 GMT)

Consensus Forecast, Retail Sales - M/M: 0.3%

Consensus Range, Retail Sales - M/M: -0.4% to 0.5%

Consensus Forecast, Ex-Vehicles - M/M: -0.1%

Consensus Range, Ex-Vehicles - M/M: -0.5% to 0.5%

Consensus Forecast, Ex-Vehicles & Gas - M/M: 0.3%

Consensus Range, Ex-Vehicles & Gas - M/M: 0.2% to

0.5%

Sales expected up 0.3 percent with sales ex-autos down 0.1

percent, not impressive results given these numbers are not adjusted for higher

prices.

US Philadelphia Fed Manufacturing Index for July (Thu

0830 EDT; Thu 1230 GMT)

Consensus Forecast, Index: 14.0

Consensus Range, Index: 5.0 to 15.0

The index is seen higher at 14.0 in July versus 10.3 in

June.

US Business Inventories for May (Thu 1000 EDT; Thu 1400

GMT)

Consensus Forecast, M/M: 0.3%

Consensus Range, M/M: 0.1% to 0.6%

Inventories expected up 0.3 percent in May after a big 0.5

percent rise in April.

US Housing Market Index for July (Thu 1000 EDT; Thu 1400

GMT)

Consensus Forecast, Index: 35

Consensus Range, Index: 34 to 37

Home builder sentiment expected flat at a gloomy 35 in July.

US Pending Home Sales Index for June (Thu 1000 EDT;

Thu 1400 GMT)

Consensus Forecast, M/M: 0.0%

Consensus Range, M/M: -0.5% to 0.9%

The consensus looks for sales flat in June after a

remarkable 3.8 percent jump in May.

Friday

Eurozone HICP for June (Fri 1100 CEST; Fri 0900 GMT; Fri

0500 EDT)

Consensus Forecast, HICP - M/M: -0.1%

Consensus Range, HICP - M/M: -0.1% to -0.1

Consensus Forecast, HICP - Y/Y: 2.8%

Consensus Range, HICP - Y/Y: 2.8% to 2.8%

Consensus Forecast, Narrow Core - Y/Y: 2.4%

Consensus Range, Narrow Core - Y/Y: 2.4% to 2.4%

The consensus looks for no revision in the final from the

flash report at increases of 2.8 percent for HICP and 2.4 percent for narrow

core HICP from a year ago. The month on month HICP is seen revised down to

minus 0.1 percent from plus 0.1 percent reported previously as energy costs

fell back in June.

US Housing Starts and Permits for June (Fri 0830 EDT;

Fri 1230 GMT)

Consensus Forecast, Starts - Annual Rate: 1.320 M

Consensus Range, Starts - Annual Rate: 1.140 M to

1.350

Consensus Forecast, Permits - Annual Rate: 1.400 M

Consensus Range, Permits - Annual Rate: 1.380 M to 1.430

M

Starts seen recovering to 1.320 million unit rate in June

from a dismal 1.177 million in May.

US Imports and Export Prices for June (Fri

0830 EDT; Fri 1230 GMT)

Consensus Forecast, Import Prices - M/M: -0.3%

Consensus Range, Import Prices - M/M: -0.8% to 0.3%

Consensus Forecast, Import Prices - Y/Y: 7.0%

Consensus Range, Import Prices - Y/Y: 6.0% to 7.2%

Consensus Forecast, Export Prices - M/M: 0.8%

Consensus Range, Export Prices - M/M: 0.6% to 0.9%

Import prices seen down 0.3 percent on the month and export

prices up 0.8 percent.

US Industrial Production for June (Fri 0915 EDT; Fri 1330

GMT)

Consensus Forecast, Industrial Production - M/M: 0.2%

Consensus Range, Industrial Production - M/M: -0.3%

to 0.4%

Consensus Forecast, Manufacturing Output - M/M: 0.2%

Consensus Range, Manufacturing Output - M/M: 0.1% to

0.3%

Consensus Forecast, Capacity Utilization Rate: 76.2%

Consensus Range, Capacity Utilization Rate: 75.9% to 77.5%

Industrial output seen up 0.2 percent on the month and

manufacturing up 0.2 percent too.

US Consumer Sentiment for July (Fri 1000 EDT; Fri 1400

GMT)

Consensus Forecast, Index: 51.3

Consensus Range, Index: 50.0 to 52.0

The consensus sees sentiment up to 51.3 in the first July

reading from 49.5 in June and up from 44.8 in May. That more optimistic reading

for July would precede the impact of latest uptick in gas prices in the last

few days.

|